Weekly Innovation Review (WIRE) #18

Latest News from the World's Leading Innovators

Headline Developments

Tesla (TSLA) has taken a $1.5b cash position in Bitcoin; catalysing a 22% rally in the digital currency. In a filing to the SEC, the company said it has done so to provide more flexibility to diversify and maximise returns on its cash, whilst leaving the door open to acquiring and holding more digital assets over the long-term. Furthermore, Tesla stated that they “expect to begin accepting bitcoin as a form of payment for our products in the near future”.

Meanwhile, Mastercard (MA) have put their weight behind the digital currency saying in a blog post that digital assets are becoming a more important part of the payments world and that the trend is “unmistakable”. In light of this, Mastercard announced that this year they will “start supporting select cryptocurrencies directly on our network”. Whilst not specifying which assets will be accepted, they did say that they expect widespread support for “crypto-assets that offer reliability and security” and that it is “those very same stablecoins that we expect to bring into our network”. A stablecoin is traditionally ‘pegged’ to a cryptocurrency, fiat money or commodities (i.e. Facebook’s Diem, Tether, USD Coin and Dai, which runs on the Ethereum blockchain).

Details have now been released on Elon Musk’s $100m XPrize inviting innovators and teams to create and demonstrate solutions that can pull CO2 directly from the atmosphere. The aim is to help remove up to 6 gigatons of CO2 per annum by 2030 and 10 gigatons by 2050 - the amount estimated to avoid the worst effects of climate change. Further details are available here and for a quick understanding of why this is important, take a look at the graphic below from Our World in Data showing the extraordinary acceleration in CO2 emissions in our lifetime!

This week, California released the 2020 disengagement report which shows progressed companies are in their AV ambitions. They do this by assessing total miles driven by the AV (with a human safety driver behind the wheel) relative to the number of times that human safety driver has had to take control (disengagement). There are 29 AV permit holders who reported to the Department of Motor Vehicles and, below, you can see all companies who have clocked more than 10,000 miles relative to the number of disengagements. On this basis, General Motors (GM) Cruise and Google’s (GOOG) Waymo is WAY ahead of the competition. But, they did have a very good head start. You’ll see a few Chinese companies scaling up plus some early miles being logged by Lyft (LYFT), Amazon’s (AMZN) Zoox and Apple (AAPL). Daimler’s (DAI.DE) Mercedes is also in the mix but had one of the worst disengagement rates with the safety driver having to take over every 26 miles vs every 30k miles for Cruise and Waymo.

Samsung (005930.KS) is deliberating over the location of a US-based chip plant, estimated to cost upwards of $17b. Austin (which has recently lured HPE, Oracle and Tesla) is being considered for one of the locations where they are seeking combined tax subsidies of $805m over 20 years for the manufacture of its more advanced chips used by the likes of Qualcomm, Nvidia and Tesla. Early last year Taiwan Semi (TSM), who control the lion’s share of the chip market, said they would build a $12b plant in Arizona. This all comes at a time of vast global chip shortages, impacting all key manufacturers from General Motors through to Sony’s Playstation.

On the topic of semiconductors, Nvidia (NVDA) competitor Graphcore (private), which has raised close to $700m from Dell, Bosch and BMW, has asked the UK regulators to block its rival’s acquisition of Arm. "If Nvidia can merge the Arm and Nvidia designs in the same software, then that locks out companies like Graphcore from entering the seller market and entering a close relationship with Arm," a Graphcore investor, said. Nvidia has previously said they will ensure independence to prevent such scenarios arising, however, it’s a struggle to see how they could actually enforce this.

It’s been a bad week for Hyundai’s (005380.KS) with the auto-maker having to furiously backpedal on earlier reports that they, and subsidiary Kia, are in talks with Apple (AAPL) on the development of an autonomous electric vehicle. In a statement to the exchange, they said they are receiving cooperation requests from “various companies” and that they are “not having talks with Apple on developing autonomous vehicles”. As recently as last week it was reported that a deal was close to being finalised.

Other Developments

TikTok (private) are following other social media peers in scaling out its e-commerce offering and monetising a highly engaged millennial and Gen Z user base. New features will include self-service advertising, affiliate links (allowing influencers to link to brands) and in-app brand catalogues.

ExOne (XONE) has launched the world’s fastest, office-safe metal 3D printer. The printer will be launched in partnership with Canada’s Rapidia (private) whose technology was the first to allow water-bound metal and ceramic parts to go directly from the printer to furnace with a debinding, significantly accelerating print production. Under the arrangement, ExOne has a right of first refusal (first dibs) for majority ownership of Rapidia.

VanEck has launched an ETF to invest in social-media hyped stocks. The social sentiment ETF (called the “Buzz NextGen AI US Sentiment Leaders Index”) will invest in stocks that most people are talking up on social media sites such as Reddit, Twitter, Facebook and financial platforms like StockTwits, Yahoo Finance and The Street. The fund pulls data from these (and many other) sites and uses AI to “identify patterns, trends and changing sentiment”. The fund invests in a whopping 75 companies including Virgin Galactic, Facebook, Moderna, Zoom and Apple (which would effectively make it a Nasdaq tracker).

Reddit (private) has seen its valuation double to $6b after raising over $250m in a recent funding round. The company, buoyed by a surge in activity on ‘meme stocks’, decided now was the right time to invest further in the company, to launch it further in international markets and broaden its video, advertising and consumer products. Reddit has more than 50m DAUs, with advertising revenue rising 90% in the last quarter (YoY).

Toyota (7203.JP), which has long resisted the EV in favour of the hybrid, has finally announced that they will be releasing two EVs for 2022. Although details are scarce, it is expected that one of the EVs will be a Toyota and another, likely a Lexus SUV or crossover.

IPOs

Bumble (BMBL) has hit the public markets, surging to $70 - 60% above the $43 issue price. This brings in $2.15b for the dating app. Revenues for 2021 are on track for ~$550m which would put the company on a fwd P/S of 18x - in line with its closest competitor Match Group (MTCH) which, by comparison, is turning over a healthy Net Profit and Free Cash Flow after years of oversight by Vimeo and ANGI Homeservices owner IAC Corp (IAC).

Battery-cell startup Freyr (private) will list on the NYSE via a SPAC deal. The Norwegian company, to be renamed Freyr Battery, expects to receive $850m as part of the merger to proceed with plans to install a battery cell production capacity of up to 43 GWh in four years. The company count Glencore (GLNCY) as an investor, who has also previously signed a deal to supply “up to 3,700 tonnes of high-grade sustainably-sourced cobalt metal cut cathodes”.

Micromobility startup Helbiz (private) is jumping on the ever-growing SPAC bandwagon, merging with GreenVision Acquisition Corp (GRNV) and valuing the company at ~$400m. In the announcement, CEO Salvatore Palella said they will be expanding their products as a last-mile solution (which has 2.7m users), further announcing plans to establish “ghost kitchens” in Milan and Washington DC later this year.

Matterport (private), which creates immersive digital twin software, is going public in a SPAC deal valuing the company at $2b. Matterport’s 3D technology is used in more than 130 countries by firms like Redfin and Marriott; with the most common use-case being 3D property walkthroughs. The company’s shareholders include Qualcomm, CBRE, AMD and Ericsson.

Electric truck maker Xos Trucks (private) is in talks to go public via a merger with NextGen Acquisition (NGAC), which would value the company at around $2bn. Xos’ (previously called Thor) competitors in this space include Nikola Motors and Tesla as well as the more established OEMs including Daimler (DAI.DE) with their upcoming Freightliner eCascadia and Geely (175.HK) owned Volvo’s VNR Electric.

Finally, Amazon (AMZN) backed EV maker Rivian (private) is seeking an IPO in September, which would value the company at ~$50bn. Rivian have signed deals with companies like Amazon and their other investor Ford (F) to supply them with delivery trucks and an EV platform respectively. To date, Rivian have raised $8.2b from ~14 investors.

M&A | Cap Raise | Earnings

DoorDash (DASH), which spruiked its focus on emerging tech and automation in its recent IPO, has announced the acquisition of Chowbotics (private) a meal prep robot/vending machine (screen grab below). Chowbotics machines are available across a wide range of industries including Grocery, Healthcare and Higher Education.

Electronic Arts (EA) is acquiring mobile game developer Glu Mobile (GLUU) in a deal worth $2.4b; roughly 35% higher than last trading levels. Glu’s gaming portfolio includes Kim Kardashian: Hollywood, Tap Sports Baseball and a Taylor Swift social network.

The FT reported that Microsoft (MSFT) made an approach to buy Pinterest (PINS) in recent months. According to the report, negotiations are not active and neither company are willing to make any comment. This would be a great deal for MSFT if it happened, however, there are a number of hurdles which would have to be overcome. Firstly, the Biden Administration’s hesitance towards further tech consolidation at the big end of town and likely shareholder pushback (many of whom have ridden a 7x surge since March last year). If PINS e-commerce and monetisation strategy goes according to plan, ARPU will only continue to accelerate, meaning MSFT would have to act fast to acquire PINS which is already trading at 19x fwd sales (with a market cap now exceeding $50bn).

Match Group (MTCH) are paying $1.73b in cash and stock for South Korea’s Hyperconnect whose two apps, Azar and Hakuna Live, allows users to connect with each other over language barriers. Azar is focussed on one-to-one video chat whilst Hakuna offers online live broadcasts. However, beyond this, Hyperconnect is a genuine technology company, building the first mobile version of the now well-deployed WebRTC standard which enables videos to be broadcast directly between users without going through Hyperconnect servers. They also offer real-time translation in speak and text, thanks to Google Cloud.

Renesas (6723.JP) are buying German chip designer and Apple supplier Dialog Semiconductor (DLG.DE) for $5.9 billion. This adds to a hefty period of consolidation in the semiconductor industry led by NVIDIA’s proposed acquisition of Arm for $39b, AMD’s acquisition of Xilinx for $37b, Marvell’s $10bn acquisition of Inphi and SK Hynix’s $9b acquisition of Intel’s NAND SSD operations. We expect consolidation to continue to accelerate in this sector so watch this space!

Softbank (9984.JP) is investing $900m, via convertible debt, in Pacific Biosciences (PACB), a global leader in end-to-end genetic sequencing from sample prep, through to sequencing and data analysis. "This strategic investment by SoftBank validates our leadership position in the long-read DNA sequencing market and enables us to further accelerate our growth strategies", said Christian Henry, President and Chief Executive Officer of Pacific Biosciences.

MKS Instruments (MKSI) have put in a counterbid for photonics and laser company Coherent (COHR), which is currently subject to an offer from Lumentum (LITE). Both deals are a combination of cash and scrip (stock) with the MKS deal worth $225 v Lumentum’s $203. The stock is trading at $221.

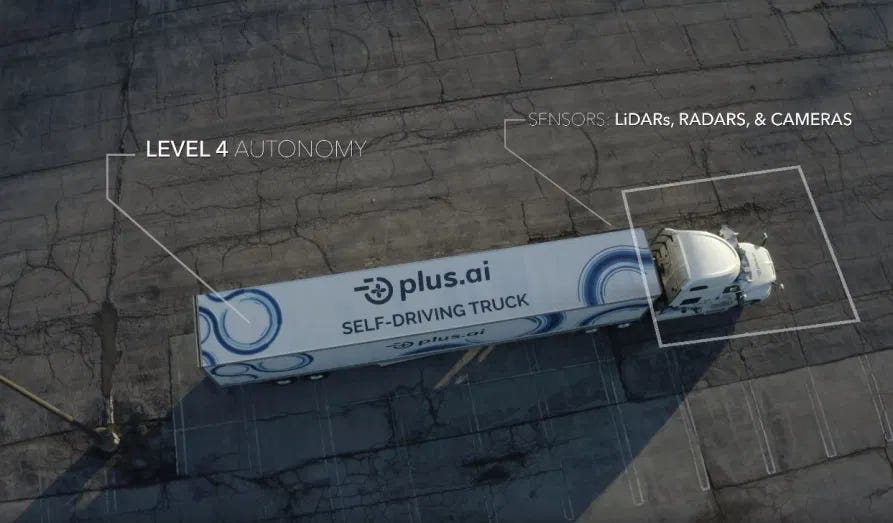

Autonomous truck company Plus.ai (private) has raised $200m from Australia’s CPE Capital, UK’s Hedosophia plus Sequoia, Mayfield and a group of Chinese funds. Plus have developed an Advanced Driver Assistance System (ADAS), called PlusDrive, which not only automates driving but improves fuel efficiency using proprietary algorithms. The funding from China helps the company expand in that country where PlusDrive they are collaborating with FAW (the world’s largest truck maker). The platform is live as of 2021.

Lyft (LYFT) shares were buoyed after an impressive set of 4Q results that beat analysts expectation. Revenue hit $570m (v $562m forecast) whilst Loss Per Share hit 58c (v 72c expected). Importantly, cost-cutting targets have been hit and, despite a 45% decline in active riders due to Covid (below), the market is anticipating a solid recovery.

Have a great week.

Charlie and Vishal

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.