Weekly Innovation Review (WIRE) #23

Latest News from the World's Leading Innovators

Headline Developments

Tesla’s (TSLA) truck hit the track this week. It is expected that it will reach ~100km/h in 20 seconds with a 36k kg load (or 5 seconds with no load!) and cost ~$150k for a 483km range or ~$180k for the 805km range, which would get you from Melbourne to (the outer suburbs of) Sydney. The truck, which has thousands of orders in place from PepsiCo, Walmart, FedEx, DHL, UPS etc has missed production targets multiple times but is now planning on a production kick off this year.

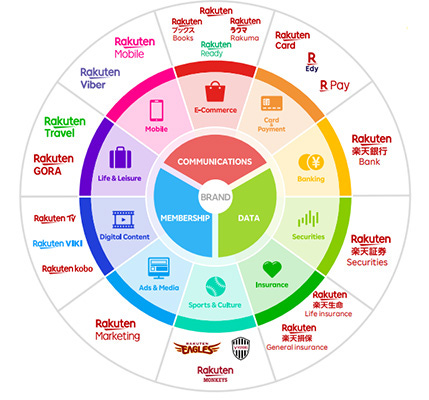

Japanese conglomerate Rakuten (4755.JP) rallied 30% this week after issuing $2.2bn worth of new shares to Japan Post (6178.JP), Tencent (700.HK) and Walmart (WMT), respectively holding 8.3%, 3.6% and 0.9%. Hiroshi Mikitani, Rakuten’s founder, chairman and CEO, said Japan Post is planning on partnering in logistics, mobile and payments whilst “Tencent opens a broad portfolio of opportunities, from digital entertainment, including online games, to e-commerce”. Rakuten generates ~54% of its revenue from internet services (e-commerce, content, media), 33% from fintech (payments, banking, securities and insurance) and 13% from mobile (telecommunications), all outlined in the below graphic.

Other Developments

General Motors (GM) is partnering with SolidEnergy Systems (SES, private), a company in which it has previously invested, to build a prototyping facility for high-capacity pre-production batteries for 2023. SES has developed an “anode-free” lithium metal battery (Li-Metal) with >400 watt-hours / kilogram (wh/kg) and >1,000 watt-hours / liter (the energy density). Today’s Li-ion EV batteries are at around 280 wh/kg and 700 whl/l. If all goes according to plan, this could give GM significantly greater mileage (up to 40% more) than leaders like Tesla (TSLA). Or it means the overall car weight can come down (the Tesla battery is ~540kg), improving efficiency and acceleration. The below is a graphic of SES’ Beyond Li-ion Li-Metal battery vs incumbents.

Not to be outdone, Volkswagen’s (VOW3.DE) announced at “Power Day” that it would reduce the cost of producing its batteries by up to 50%, building multiple battery factories around the world and expanding its network of charging stations. VW’s aim is to reduce the cost of battery production below $100/wKh (which would bring costs in-line with combustion engines). On the charging-front, VW will partner with BP (BP) to establish ~8k fast-charging points throughout Europe (mostly Germany and the UK) at 4,000 BP and ARAL fuel stations. On the production side, VW’s batteries are currently built by LG Chemical (051910.KS), Samsung (005930.KS) and China’s CATL (3000750.SZ), with future production to pull in SK Innovation (096770.KS) and, eventually, VW-backed Li-Metal startup QuantumScape (QS).

You may also recall that LG Chemical (051910.KS) are in the process of spinning off its EV battery business into a separate unit. Well….that’s had a little bit of a bump with proxy advisors ISS and Glass Lewis both recommending shareholders reject the spinoff plan, saying there is no compelling reason for the transaction and there was “inadequate rationale”. Hedge fund Whitebox Advisors claims the spinoff aims to resolve a family succession issue to the determinant of minority shareholders.

BMW (BMW.DE) plans to have 25 electric cars by 2025, with the BMW iX SUV and BMW i4 sedan being the first off the production line. Both will have the new 8th generation iDrive platform (in the feature image of this post), centred around a 14.9-inch touchscreen (vs Mercedes’ 56 inch hyperscreen!). Range-wise they’re middle of the ground, hitting 300 miles on a single charge, with the i4 going from 0-100km/h in four seconds.

Lucid Motors (private) are collaborating with Dolby Labs (DLB) to bring Dolby Atmos audio to the upcoming Lucid Air. Lucid’s Surreal Sound System will come standard in the company’s premium in the Air Grand Touring and Air Dream models. To get the most of the technology, customers will need access to a high-res music subscription from the likes of Amazon, Deezer, Tidal and, presumably, Spotify (when they start rolling out their high-res subscription).

Nokia (NOK) has announced a partnership with Microsoft (MSFT), Amazon (AMZN) and Google (GOOG) to develop cloud-based 5G radio solutions with its radio access network (RNA) technology. “Open collaboration is key to the development of new and innovative high value 5G use cases that will equip our customers with the tools they need for digital transformation,” Nokia President of Mobile Networks Tomi Uitto said.

A couple of policy considerations coming out of India are worth highlighting this week. Firstly, the Government have drafted an e-commerce policy to ensure companies like Amazon (AMZN), Walmart’s (WMT) Flipkart (pending listing) and Reliance’s (RELIANCE.NS) JioMart treat sellers equally on their platform. Reuters have reported in the past that Amazon flouted regulations by by-passing small Indian retailers for a few big sellers (i.e. 35 of Amazon’s 400k sellers in India accounted for two-thirds of sales).

Separately, and as we reported a few weeks ago, India is considering a bill that would criminalise possession, issuance, mining, trading and transferring of crypto-assets. Reports indicate that crypto holders will have six months to liquidate their assets before a penalty is levied. It is expected that 7m citizens in India have invested $1bn in cryptocurrency (not even a blip on the radar compared to the estimated $1.6 trillion crypto market size).

Geely (175.HK) is spending $4.6bn on an electric battery plant in Ganzhou, China. The factory will have a capacity of 42 GWh per year - similar in size to what Germany’s Volkswagen (VOW3.DE) said it would build in Europe. Geely’s factory plans come two months after the company announced it would team up with Baidu (BIDU) to manufacture intelligent electric cars.

IPOs

Trading platform eToro (private) is following in the footsteps of Robinhood, merging with FinTech Acquisition Corp (FTCV) in a SPAC deal. The deal is expected to close in 3Q with an implied equity value of $10.4bn and private placement commitments (to the tune of $650m) from ION Investment Group, Softbank, Third Point and Fidelity. eToro has 20m registered users across 100 countries who use the platform's social trading functionality to copy portfolios of popular investors (who receive up to 2.5% of followers funds or AUM as payment). So, if you pull in the minimum $10m AUM for Elite Pro (which needs 10 people copying your portfolio), you’d earn yourself a nice $250k/year.

According to the WSJ, Singapore’s Grab (private) is looking to accelerate its path to market via a SPAC. This would put a $40bn price tag on the ride-hailing company - 2x Lyft and 0.40x Uber. As part of such a deal Grab would raise $3-$4bn in a PIPE (private investment in public equity) deal. Grab, which started as a ride-hailing startup back in 2011 has morphed into an SE Asian super-app, expanding into delivery (GrabFood, GrabExpress) and financial services (GrabPay, GrabFinancial) with $12.1bn in venture backing from the likes of Softbank (9984.JP), Hyundai (005380.KS), Toyota (7203.JP) and Vertex Ventures.

US-digital bank Chime (private) is targeting a public debut with a valuation of ~$30bn according to Reuters. Chime’s CEO Chris Britt says the company is looking at all potential paths including an IPO, direct listing or SPAC. Chime, like the myriad other neobanks, is hugely popular with younger generations with features like fee-free overdraft (up to $100) and advanced pay (up to 2 days early). However, for now, there are no loan or mortgage products which, as we saw with Xinja in Australia, is a bank-killer (i.e. no interest income to offset the interest expense).

Korean bioprinting manufacturer Rokit Healthcare (private) is preparing to list on the domestic stock exchange, as it looks to strengthen the development of its 4D bioprinting innovation. One of the company’s current innovations takes a patient's fat tissue to form a bio-ink, which is then loaded into the company’s Dr. INVIVO DFU 4D bioprinting platform, producing a dermal patch to heal and close diabetic foot ulcers (DFU). This innovation has seen a 100% strike rate in wound healing on tested patients in Korea and India. They are also looking at treating osteoarthritis via cartilage regeneration treatment and are in the process of pre-clinical studies for a HumaTein Skin Spray to treat burn injuries.

Chinese AI company Megvii (private) is preparing for a $1bn listing on China’s STAR Market (their Nasdaq). We don’t usually report on mainland listings, however, Megvii is an interesting one as its facial recognition platform, Face++, monitors residents in over 100 Chinese cities in order to maintain “social stability”. Of most concern is the company’s role in the reported surveillance of Muslim minority groups in Xinjiang - leading to the company being cut-off by the US Government. Alibaba (BABA) and subsidiary Ant Group (private) own 29.4% of the company with other investors including Australia’s Macquarie Group (MQG.AX). I wonder how that investment slipped through Macquarie’s ESG filter!

DigitalOcean (DOCN), which provide a suite of cloud solutions like website hosting, apps, video streaming, big data and game development, will list on the NYSE in the coming weeks. The company, whose clients include GitLab, Slack and Splunk, will be valued at ~$4.8bn. Unlike AWS, DigitalOcean is focussed on simplicity, offering a handful of products, including customisable Linux-based virtual machines (called droplets), data storage options, networking tools and three databases. In a dig at Amazon/Google/Azure, DigitalOcean has said their (the big guys) products aren’t intuitive enough for small businesses and suffer from “near-infinite feature complexity” with “significant hidden costs”.

Californians consumer electronics brand Vizio (VZIO) will hit the NYSE with a target valuation range of $4.2bn. Vizio makes smart TVs and soundbars and has developed a smart TV operating system called SmartCast. Financially, the company pulled in $102m in Net Income off $2bn in revenues in 2020.

M&A | Cap Raise | Earnings

Cruise (private), the autonomous vehicle startup backed by General Motors (GM), Honda (7267.JP) and Microsoft (MSFT) will be buying AV startup Voyage (private). Voyage is one of the smaller operators in the AV space, however, the acquisition adds ~60 employees and a depth of IP from various autonomous operations in senior living communities. Cruise founder, Oliver Cameron, will take on a new role as VP of Product at Cruise, as it pushes towards commercial robotaxi operations.

Qualcomm (QCOM) just closed its acquisition of Nuvia (private) for $1.4bn. Importantly, this brings an incredible amount of talent to Qualcomm, with Nuvia’s founders being ex-Apple chip designers. Specifically, Gerard Williams was Apple’s chief CPU architect for a decade, responsible for the chip that’s been in every iPhone since the 5S, according to Gizmodo. In closing the deal, Qualcomm announced that the IP will be encompassed within their internally designed CPUs and SOCs from 2H22 - applicable to high-performance ultraportable laptops.

Snap Inc (SNAP) is furthering its push into e-commerce with the acquisition of Fit Analytics (private), a company that uses machine learning to match a customer’s dimensions to clothes and shoes with the best fit. There are currently 18,000 retailers using the platform including North Face, Asos, Calvin Klein, Patagonia and Puma. According to Fit Analytics CEO and co-founder Sebastian Schulze, their main goal will be to “grow their shopping platform, leveraging our technology and expertise.” Specifically, the AR capabilities of Snap, when overlaid with the ML capabilities and database of Fit Analytics has the potential to revolutionise Snap’s e-com customer experience. Stitch Fix (SFIX) offers a similar platform for CK, O’Neill, Toms and Michael Kors (and >1,000 other brands).

Stripe (private) has hit an eye-watering $95 billion valuation after raising $600m in funding from a large group of investors including Allianz (ALV.DE), AXA SA (CS.PA) and Fidelity. This makes it the most valuable US startup, surpassing Elon Musk’s SpaceX (at $74bn). The price tag also makes Stripe bigger than any bank in Europe, which accounts for 31 of the 42 global markets in which Stripe is active. The capital will be used for the expansion of those European operations on top of a broader global expansion of its payments and treasury network.

Squarespace (private), which filed to go public recently, has raised $300m in a round of funding, valuing the company at $10 billion. New backers include Dragoneer, Tiger Global and Fidelity joined existing investors Accel and General Atlantic in the round.

Crowdstrike (CRWD) reported 4Q earnings this week beating consensus estimates. 4Q revenue came in at $264.9m +74% you and 6% ahead of market expectations. Non-GAAP subscription GM hit an impressive 80% and free cash flow margin 37% (who said SaaS businesses don’t generate cash?). Excellent guidance for FY22 (Jan 22 YE) at +51% YoY growth again ahead of consensus estimates. The cybersecurity firm added a record 1,480 net new subscription customers in the quarter. Its annual recurring revenue (ARR) surpassed the $1 billion milestones.

Have a great week.

Charlie and Vishal

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.