Weekly Innovation Review (WIRE) #27

Latest News From the World's Leading Innovators

A much longer edition of WIRE this week thanks - in part - to NVIDIA’s investor day which has to be covered off to some degree! Arguably, they are the world’s leading innovator!

Headline Developments

Coinbase (COIN) rocketed nearly 60% on its market debut, giving the company a market cap in excess of $100bn; before settling back towards $86b. If the company continues its strong 1Q growth then implied sales for 2021 will be ~$8b - putting the stock on a 10.75x fwd P/S. Like almost anything to do with crypto, the listing is polarising, however, from a pure financial perspective, that 10.75x multiple does make it cheaper than equity trading platform Interactive Brokers (IBKR) which likely has more subdued growth prospects. The bulls would argue that Coinbase’s growth will continue in-line with the unabated demand for crypto (nb. COIN control 11.3% of the crypto market). The bears, however, will look at this market volatility and the prospect of regulatory action (raised by crypto-exchange Kraken’s CEO) and take several steps back.

A big win for the Biden administration, with South Korea’s LG Chemical (051910.KS) and SK Innovation(096770.KS) pledging to work together to strengthen the EV battery supply chain in the US and support Biden’s efforts to advance clean energy policy. This comes after the US International Trade Commission’s February decision that SK stole 22 trade secrets from LG Energy, and that SK should be barred from importing, making or selling batteries in the US for 10 years. This decision would have been a major hindrance to the pro-EV policies, disrupting automakers like Ford and VW and putting at risk a $2.6b SK battery factory under construction in the state of Georgia. As you can see in the below graphic from South Korea’s SNE Research, domestic suppliers LG Chem, SK Innovation and Samsung SDI control 42% of the EV battery market worldwide, with Tesla supplier Panasonic (6752.JP) controlling 34% and China’s CATL and BYD ~10%.

Whilst on the topic of batteries, Amazon (AMZN)-backed EV company Rivian (private) have locked in Samsung SDI as their battery supplier. You may recall from previous editions of WIRE that Rivian is pushing itself as the brand for adventurers with extensive testing of battery tech in extreme conditions (i..e -40f). The selection of Samsung SDI (006400.KS) is a big show of faith in the South Korean conglomerate to deliver the performance consumers (and shareholders) are depending on.

China has fined Alibaba (BABA) $2.8b after finding the company had violated anti-monopoly law. The Chinese Government had launched its investigation back in December to determine whether the company was preventing merchants from selling their products on other platforms. The Government found that Alibaba had (surprise surprise!) used algorithms to strengthen its own position in the marketplace. They will have to make moves to reduce these tactics and provide compliance reports periodically over the next three years.

Other Developments

Let’s kick off with a lengthier than normal update from NVIDIA’s (NVDA) annual investor day - now the most important annual update purely due to the significance of NVIDIA’s technology across the entire technology landscape. If you need a refresher on the semi industry first, feel free to read this piece where I’ve provided an easy to read summary of the industry (who’s who and what’s what)!

There’s a lot to take in so I’ve broken this down one by one:

Release of their first data centre CPU “Grace” (below) built on the Arm architecture and comprising a number of NVIDIA GPUs and Arm-based CPUs for highly advanced AI applications and language processing. This is a big kick in the guts for Intel who have traditionally dominated the data centre CPU market and are now in a serious struggle to maintain an edge over competitors

A new data processing unit (DPU) called BlueField 3 with 10x the compute power of prior generations [nb. NVIDIA’s data centre roadmap comprises GPUs, CPUs and DPUs which the company will evolve rapidly year to year]

AI-on-5G computing platform will be the most advanced edge computer ever created. Initial partners include Fujitsu, Google, Mavenir, Radisys and Wind River

NVIDIA Omniverse - a platform for real-time simulation in 3D [nb. a demo was done with BMW showing a real-time digital-twin of one of their factories, below]

Finally, NVIDIA’s DRIVE platform is amplified with the DRIVE Atlas SoC; delivering 1,000 trillion operations per second (TOPS). To put that in perspective, it’s 40x more efficient than Qualcomm’s (QCOM) Snapdragon 888 which will power most new android phones

NVIDIA also announced all the new kids on the auto-block are signing up with DRIVE - including Canoo (GOEV), Faraday Future (pending listing), Vietnam’s Vinfast (private), Nio (NIO), Li Auto (LI), XPeng (XPEV) and SAIC (600104.CH).

You can see a little summary of all of this below:

But….where does this leave Intel’s (INTC)? Well….all of these announcements are frankly ominous. The semiconductor pioneer has a new leadership team and is drastically trying to pivot and open its fab capabilities to outside customers. However, by the time this comes on board the ship may have already sailed. It would be a brave investor to back Intel over NVIDIA over the next decade. But stranger things have happened!

Let’s move on from Intel and NVIDIA and talk about autonomous pizza delivery.

That’s right, Nuro (private) will start delivering Dominos (DPZ) pizza in Houston as part of a pilot program. Select customers who make a pre-paid delivery order can elect to receive their delivery from Nuro’s R2 robot, receiving a unique PIN via SMS which is then entered on a touchpad once the R2 arrives. CVS’ (CVS) Pharmacies are also doing deliveries from select stores in Houston using the R2.

The rumours we reported last week, about a Spotify (SPOT) device called Car Thing has actually turned out to be a thing, and you can join the waitlist here “if Car Thing” becomes available (not when!). The product below doesn’t require much explaining. It’s a smart-phone looking device purely for listening to music, with voice-command, that sits on the dashboard. Pricing-wise it’s only $80. It’s not something that will significantly move the needle for Spotify in terms of revenues, however, does show a real intent by the organisation to innovate and push into the physical product category.

Spain has budgeted €400m (with room to expand to €800m) for EV subsidies. This means that purchase of EVs in the country is now subsidised with €7k (if an older car is scrapped) or €4.5k without scrapping. Other conditions for the subsidy require cars to have a range of at least 90kms with the car value not exceeding €45k (so this is a max 10-15% subsidy). All major developed countries in the world (US, UK, Spain, Canada, China, India, Japan) offer some EV incentive with the one glaring omission being Australia who, despite some marginal stamp duty discounts, actually tax you for driving an EV (to make up for lost fuel excise)!

Loral Space’s (LORL) 63% owned Telesat is expected to finalise financing shortly for its Lightspeed broadband constellation, along with contracts to launch the fleet of ~300 satellites. The roll-out is expected to cost $5b and kick off in 2022. The coming decade will see tens of thousands of satellites and nano-satellites hit Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) led by Elon Musk’s SpaceX (private), Amazon’s (AMZN)Project Kuiper, SES Networks (SESG.PA), Viasat (VSAT), EchoStar (SATS) and OneWeb (private), the latter being recently bailed out by the UK-Government, India’s Bharti Global, Softbank and EchoStar subsidiary Hughes Network Systems. Image below of Telesat’s Phase 1 LEO satellite built by Airbus (AIR.PA) subsidiary SSTL.

From 2022, all future Sony Pictures (Sony, 6758.JP) movies will be released exclusively on Netflix (NFLX) after their cinema release. This would include the upcoming Morbius, Uncharted, Bullet Train, Spider-Man franchise and back catalogue including Jumanji and Bad Boys. This is a big deal for Netflix, particularly with competition heating up from vertically integrated streamers such as Disney (DIS) and AT&T (T) - the owner of Warner Media and its subsidiary HBO.

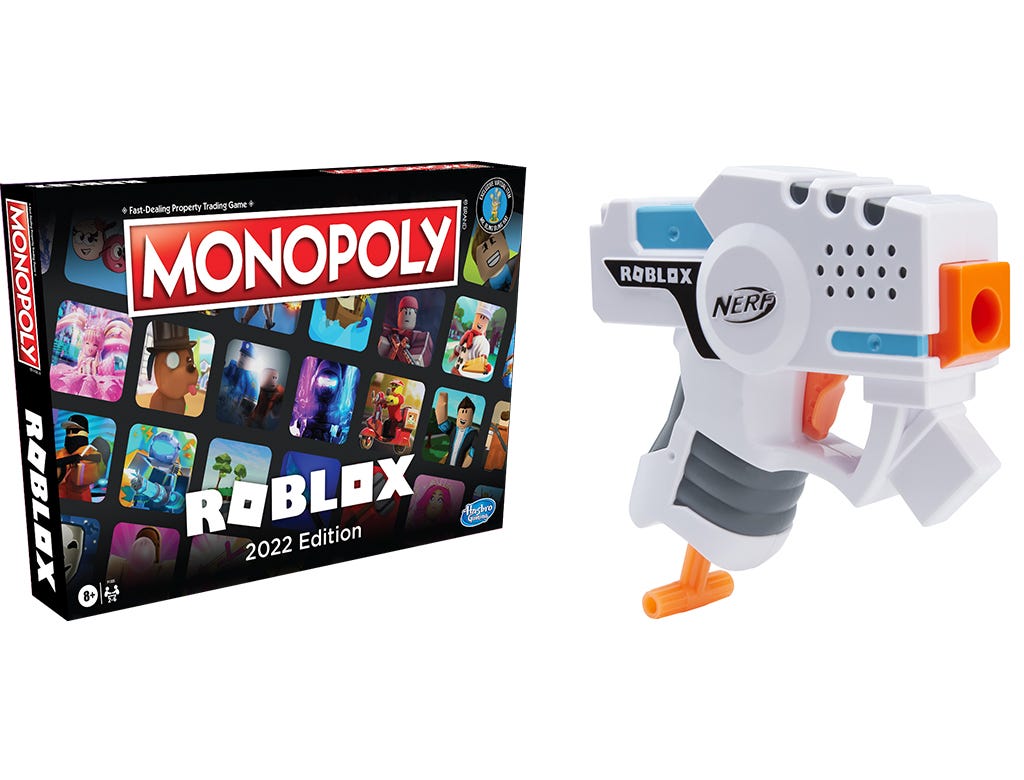

Roblox (RBLX) jumped 10% after announcing a deal with Hasbro (HAS) to bring a range of Roblox-inspired NERF blasters. When the physical blasters become available in the US this fall, they will come with a code that kids can use to redeem a virtual blaster for their avatar within the game. In addition, Hasbro has developed a Roblox version of Monopoly - available for pre-order in the US and UK here which will also allow for redemption of in-game virtual items. The $4.2b move might seem a little excessive (i.e. it could buy you 120m NERF blasters), however, it prices in a highly unique monetisation and ad revenue strategy which we’re likely at the very cusp of. Imagine Roblox redemption codes for Nike, the 49ers…..Jeep.

IPOs | SPACs

Singapore’s ride-hailing/food delivery/fintech Grab (private) will merge with Altimeter Growth (AGC), paving the way for a $40b market listing (and the biggest SPAC deal ever, nudging out the upcoming $24b Lucid deal). The company will rake in ~$4.5b in proceeds as part of the deal which is aimed to close by July, with proceeds being used to retain and expand its user base which is under continual threat from the likes of Sea Ltd (SE) and the soon to be merged Indonesian groups Gojek and Tokopedia (or “Goto”).

Self-driving truck platform TuSimple (private), backed by Goodyear (GT) Ventures, trucking company Navistar (NAV) and Volkswagen (VOW3.DE) is targeting a $7.85b IPO. The company is building what they call the world’s first Autonomous Freight Network (AFN) with over 5,700 purpose-built fully autonomous trucks reserved by fleet operators so far. In a nutshell, the AFN connects terminals adjacent to interstates before handing them over to human drivers, who will complete the more complicated ‘last mile’ delivery. Phase 1 (now) connects major cities in Arizona and Texas with Phase 2 (2022-23) expanding operations to the South East (i.e. Florida, Louisiana, Georgia) before a national rollout from 2023 onwards. The majority of revenue will be generated from per-mile fees charged to users of the AFN. You could call it Trucking as a Service (TaaS). In fact….they have.

Can cyber-security startup Darktrace (private) deliver for England after a shambolic Deliveroo (ROO.L) IPO! The numbers would say yes. The company, which uses AI to detect and respond to cyber threats, saw sales climb 45% YoY to $199m with a 90% gross margin. They are targeting a $4.1b valuation which would imply a ~14x fwd P/S (assuming the same growth rate). By comparison, Okta and Cloudflare trade ~30x fwd P/S for similar growth and a worse gross margin. Whatsmore, trust radius and G2 rate the platform 85% and 88% respectively and the company has a deep patent portfolio for cyber defence systems and threat detection (119 patents published since 2015).

UiPath (PATH) has provided further details ahead of their NYSE debut, targeting a valuation of $26b with proceeds of ~$1.06b at the upper end of the range. The company, which provides enterprise automation software for finance, healthcare, telco, retail and various other industries, saw revenue hit $607m for the 12m ended Jan-2021 - a whopping 80% jump YoY. Gross margins were also sitting around 90% with Net Revenue Retention of 153% - both super impressive metrics. Assuming it maintains that annual growth rate, the implied fwd P/S would be almost 24x for 2022.

Softbank (9984.JP) has continued its investment spree, leading a $679m Series D funding round for semiconductor startup SambaNova System (private) alongside Intel (INTC) Capital and Google Ventures. What makes SambaNova unique is that their chips are not designed on Arm or x86 (like everyone else) but on their own Reconfigurable Dataflow Architecture (RDA). These chips, which go into SambaNova servers, are then leased out to companies on a Dataflow-as-a-Service model. With Intel’s x86 architecture fading into (relative) obscurity, bets like this for their VC arm are critical.

Plant-based meat innovator Impossible Foods (private) is exploring avenues for a market listing, in a deal that would value the company in excess of $10bn. Just like Beyond Meat (BYND), Impossible Foods produce plant-based meat patties (the Impossible Burger), sausage and pork, however, they differentiate themselves by adding heme (which binds oxygen in the bloodstream). The heme, which they extract from the roots of soybean plants, is according to Impossible Foods “what makes meat taste like meat”.

Didi (private) is preparing for a US IPO according to Nikkei. As per our prior reports, the expected valuation is between $70-$100b, with capital raised from the offering to fund further global expansion. Despite Trump’s crackdown on US-listed Chinese companies (which saw a few telco delistings) there are currently 20 Chinese companies eyeing off a US-listing at present, with 20 listing in 1Q21 and 34 last year.

M&A | Cap Raise | Earnings

Microsoft (MSFT) is buying Nuance Communications (NUAN) for $19.7b. Nuance is an AI and speech-recognition firm with a particular focus on healthcare solutions such as clinical documentation, follow-up adherence as well as virtual assistant technologies. This deal expands on Microsoft’s Cloud for Healthcare and buys them an impressive and engaged customer base comprising 55% of physicians, 75% of radiologists and 77% of hospitals in the US.

Dell (DELL) was up 10% overnight after announcing that it would spin off its 81% stake in cloud-computing company VMWare (VMW); acquired as part of 2015’s $67b acquisition of EMC. Under the terms of the deal, Dell will pay an $11.5-$12b special dividend to all shareholders (including itself), with proceeds (of which $9.3-$9.7b is Dell’s) being used to pay off the parent’s hefty net debt (equivalent to ~50% of its market cap!). This, in part, is why rumours of this deal have been circulating for some time. Despite the rationalisation, both companies will continue to work very closely together. Longer-term it removes quite an overhang from VMWare’s register, and gives Dell some much needed financial breathing room!

In the midst of mounting pressure from hedge fund Starboard, Box Inc (BOX) has confirmed that PE firm KKR is investing $500m in the company. The proceeds will be used for a share repurchase of up to $500m of its common stock (~15% of the company). From KKR’s perspective, they see Box as a “highly differentiated product platform with a customer-centric vision that makes it an ideal investment” for the company.

Epic Games (private), the maker of Fortnite which is in a David and Goliath battle with Apple, has raised $1b in a deal valuing the company at $28.7b. Funding for this round has come from Sony and a who's-who of funds including T.Rowe Price, OTPP, Luxor, GIC, Fidelity, Blackrock and Franklin Templeton. CEO Tim Sweeney says the investment will “help accelerate our work around building connected social experiences in Fortnite, Rocket League and Fall Guys, while empowering game developers and creators with Unreal Engine, Epic Online Services and the Epic Games Store,” Sweeney said. We suspect part of that raise will also go towards some quite hefty legal fees (which would be more than offset if they won!).

Have a great week.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.