Weekly Innovation Review (WIRE) #30

Latest News from the World's Leading Innovators

Headline Developments

The battle is on between Fortnite developer Epic Games (private) and Apple (AAPL) - a David and Goliath case which, in a nutshell, will ask whether Apple is acting fairly by charging developers a 15-30% fee for all revenues made via subscriptions and in-app purchases. Epic argues that Apple has created a digital walled garden which makes it as difficult as possible for consumers to stop buying its products. Conversely, Apple will argue that the only reason many consumers are on the platform is because of that garden. In reality, Fortnite is creating what could be the world’s biggest Metaverse (a ubiquitous virtual space/world) and they’re not too keen to be paying an Apple tax on every single transaction within that Metaverse into perpetuity. If Epic wins, it’ll wipe a lot of value off Apple, and lift up all key gaming stocks including ‘metaverse’ peers like Roblox (RBLX)…..and every other game/app developer subject to the Apple tax!

NASA has now suspended the lunar lander contract with SpaceX (private) after the Amazon (AMZN) and Dynetics (private) tantrum last week. For a recap, NASA ran into some budgetary constraints and, according to Amazon, moved the goalposts on the Human Landing System (HLS) contract which they handed exclusively to SpaceX (who came in as the cheapest option at $2.9b). There were of course other considerations but I won’t bore you with the details! The suspension (or pause) will be in place whilst the Government Accountability Office (GAO) makes a decision (due by 4th Aug). Of course, a favourable ruling by the GAO could only really be enforced with more funding from the President (what’s an extra few billion dollars these days anyway!?).

Whilst on the topic of multi-billion dollar cheques, it’s time to talk about Intel (INTC).

As you may know, the semiconductor pioneer which is being lapped by the likes of Nvidia (NVDA) and AMD (AMD), has had a recent strategy shift to being a contract chip manufacturer (or fab) like Taiwan Semi (TSM) and Samsung (005930.KS). That’ll take a little while to show on the financials, but to help get there they’ve thrown $3.5b into upgrading a New Mexico chip plant (on top of $20b already being invested in Arizona). Intel is also going cap in hand to the EU for $9.6b in public subsidies towards building a semiconductor factory in Europe.

Separately, Taiwan Semi (TSM) is planning to build up to five more fabs in Arizona, beyond the one currently planned, according to Reuters.

Other Developments

The Clubhouse (private) hysteria is tapering off, just as Facebook (FB), Twitter (TWTR) and Reddit (private) ramp up their own audio platform. Clubhouse saw 9.6m downloads at its peak in February, with this month's figures a ‘mere’~900k. What you’re likely to see here is a brief recovery in downloads, particularly with a Clubhouse android release, but following this, it’s a struggle to see how they’ll rapidly pull users away from the majors and be anything more than a niche social tool.

But it’s not only Clubhouse that Facebook (FB) is trying to squeeze out, they’re now doing the same to neighbourhood app Nextdoor (private). The social media giant’s new tool, called Neighbourhoods, is being tested in the US and Canada and will allow users to find neighbours with similar interests, discover local groups and businesses, participate in polls and offer help to those in their communities.

Volkswagen (VOW3.DE) will be designing their own chips for self-driving cars, much like Apple (AAPL) has done with the M1 chip for their suite of consumer products or Tesla does for their current lineup (they used to buy off the shelf NVIDIA). This shift to in-house design will be a growing trend as automakers and various other OEMs look to fully customise their hardware and software stack (mostly off the back of Arm designs which lends itself more to edge than Intel’s X86).

Emerging EVco Arrival (ARVL) and Uber (UBER) are partnering to develop a purpose-built EV (The Arrival Car) for ride-hailing, with the car expected to enter production in Q323. This is part of Uber’s overarching goals to fully electrify its platform by 2025 in London, and 2030 in North America. To help with the transition in London, an escrow account/fund of $188m has been established to support drivers switching to EVs.

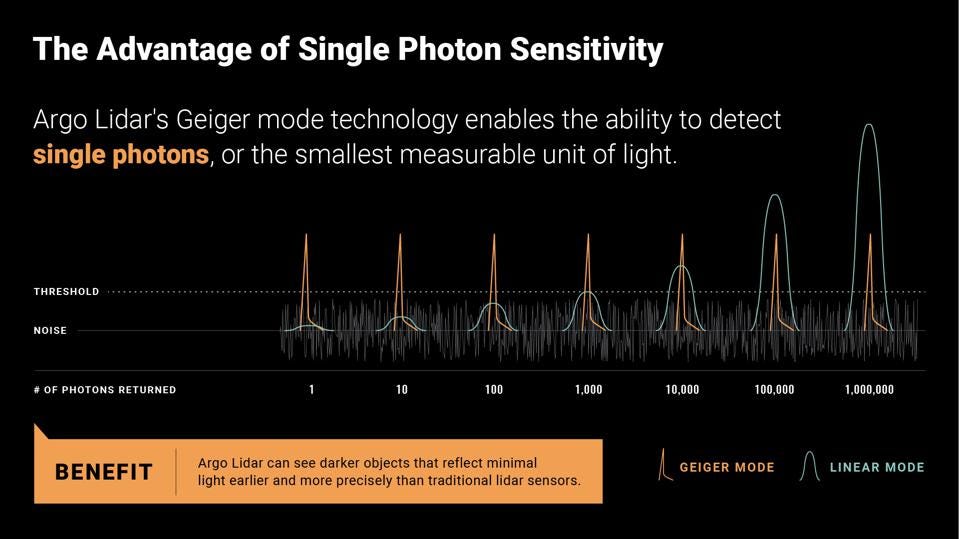

Argo AI (private), the AV company backed by Ford (F) and Volkswagen (VOW3.DE) will start rolling out its in-house designed LiDAR sensors, developed following its 2017 acquisition of Princeton Lightwave. The sensor claims a range of 400m which is well beyond the current standard of 200-300m set by the likes of Velodyne (VLDR), Luminar (LAZR), Aeva (AEVA), Ouster (OUST) and Innoviz (INVZ). How have they done this? Well, it’s a mix of longer wavelength lasers and detection technology. On the latter, a LiDAR works by shooting light and then measuring how long it took for specific light beams (once reflected from an object) to get back to the sensor. This works well in short distances but the challenge for longer distances is objects become less reflective and it’s harder to recognise reflective signals amongst the noise. Well, Argo has an array (Geiger mode - GmAPD) that solves a lot of this by detecting the smallest measurable units of light (single photons) over those long distances. It’s hard to explain in a short note so if you’d like to know more, please read this excellent article in Forbes.

On the crypto front - eBay (EBAY) CEO Jamie Iannone has indicated the company is revisiting crypto as a payment option after abandoning Facebook’s (FB) Libra in 2019. They are still at exploratory stages whilst also looking at how to gain exposure to the non-fungible token (NFT) market.

On the topic of crypto, Turkey is continuing its crackdown on the asset class after a bit of an Ocean’s Eleven style crypto heist. Last month the country said crypto couldn’t be used as a form of payment, catalysing the collapse of domestic exchanges Thodex and Vebitcoin. The 27-year-old Thodex founder, Faruk Faith Ozer, fled to Albania with ~$2b in funds belonging to his platform’s ~390k users (and now has an Interpol warrant on his head). As a result of all of this (and other activities), Turkey only recently said crypto exchanges would be regulated by anti-money laundering (AML) and terrorism regulations like other financial institutions. Such moves are becoming common as Governments around the world balance regulation, deregulated assets, tax and the adoption of their own sovereign digital currencies.

China is a little annoyed at India this week after reports indicate India had not allowed Chinese companies to conduct 5G trials in the country. India said it would allow foreign mobile carriers to carry out 5G trials with equipment makers but did not name China’s Huawei among the participants. This is hardly a surprising development given the deteriorating relationships between the two nations. This week India’s External Affairs Minister S Jaishankar said relations are going through a ‘very difficult phase’ which would be catalysed by the border conflicts at the Line of Actual Control (LAC) and, no doubt, the covid disaster which is devastating India at present. Whatsmore, India is following a growing list of nations blocking Chinese companies from their critical communications networks.

Peloton (PTON) dropped 15% after announcing it will recall two of its treadmills after discussions with the US Consumer Product Safety Commission. This follows earlier reports of injuries and one death on the treadmill! At present the incident tally has grown to 70 for the two products; the $2.5k Tread and the $4.3k Tread+.

IPOs | SPACs

Squarespace (SQSP) is readying for a direct listing on the NYSE on 19th May, with the company tracking along nicely in the lead up posting ~28% YoY revenue growth numbers (to $621m). That’s a touch under the 30% revenue growth Wix (WIX) saw over the same period (with revenues hitting $988m). That’s a 16.5x trailing P/S for Wix, which would imply a $10.2b valuation for Squarespace - in line with where it was valued during it’s cap raise earlier this year.

A big debut for British cyber-security company Darktrace (DARK.LN) with shares jumping as much as 40% on its first day of trading in the UK (stock now settling at 315 pence - 26% up from listing date). This puts it on a 15x P/S (based on $200m 2020 revenue which grew 45% YoY) - quite a steep discount to the 36x and 50x for Palantir (PLTR) and Crowdstrike (CRWD) respectively. Although Crowdstrike's growth has been at a staggering 81% (PLTR at 47%).

M&A | Cap Raise | Earnings

Sony (6758.JP) has taken an undisclosed minority stake in the gaming-focused chat app Discord (private), only a few weeks after a Microsoft (MS) deal was being thrown around. Little is known of the Sony/Discord deal other than the plan to “bring the Discord and Playstation experiences closer together on console and mobile starting early next year”. The Discord platform, which allows gamers to talk/chat to each other, currently has over 100m MAUs and has raised ~$480m to date from Tencent (700.HK), AT&T’s (T) WarnerMedia and, of course, Sony.

PayPal (PYPL) is up 4% aftermarket following a strong earnings release (EPS and Revenue 20% and 2% above estimates respectively). On the call, they also highlighted that crypto would be a key growth engine for the company, with CEO Dan Schulman saying “We’ve got a tremendous amount of really great results going on tactically with our crypto efforts” with half of crypto users opening their PayPal app daily. The company plans to roll out a nextgen crypto wallet in the third quarter - an all in one personalised app that will allow for shopping, financial services and payments experiences.

Activision Blizzard (ATVI) rallied 5% following a stunning set of results which saw revenues come in ~16% above street expectations. Much of this was thanks to the Call of Duty franchise and its 72% YoY surge in revenue (and a tripling in MAUs over three years). Their Blizzard (Warcraft) and King (Candy Crush) units saw revenues increase 7% and 22% respectively.

Lyft (LYFT) rallied to a similar degree after reporting a ‘better’ than expected loss - thanks to us, slowly but surely emerging from our covid hibernations. Active riders were 13.49m (vs 12.8m expected) whilst loss per share was 35c/share (not as bad as the 53c/share loss expected). All in all, not a terribly bad set of results, but still….a long way to go until they’re back at the 21.2m active riders they were seeing just before covid.

Have a great week.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.