Weekly Innovation Review (WIRE) #38

Latest News from the World's Leading Innovators

Headline Developments

We can now modify DNA inside of a human body (in vivo), thanks to some groundbreaking work announced this week by Intellia Therapeutics (NTLA) which saw the company’s share price surge 55%. What this means is that we can now send precision therapeutics (based on CRISPR technology) to “seek and destroy” problematic genes. In the case of Intellia, the therapy NTAL-2001 was found to reduce the level of liver disease (associated with the protein transthyretin) by 87%. According to Intellia’s President and CEO John Leonard “by developing complete solutions for both editing and delivery, we have created not just the [MVP] but a versatile, modular platform that can be applied to a broad spectrum of diseases”. As well as Intellia, it’s also worth keeping an eye on other CRISPR-based therapeutic companies like Editas (EDIT), Crispr Therapeutics (CRSP), Beam Therapeutics (BEAM) and Regeneron (REGN).

A lot of space news this week!

Kicking off with Virgin Galactic (SPCE) which rocketed almost 40% after the FAA gave it permission to start taking paying customers to space (the first-ever such license). The company has three more test flights scheduled prior to the official public launch, with Richard Branson likely to be a passenger on one of those; perhaps even beating Jeff Bezos to space if he launches by 20th July!

If you’d prefer a more relaxing (and value for money!) trip to space then perhaps Space Perspective (private) is your thing. Instead of blasting you into space for a few minutes of excitement, this company (which just started taking bookings) will let you and 8 others (including the pilot) float in space for two hours (six hours in total after a gradual ascent and descent with a balloon) as the sun creeps over the horizon. The first flights are planned for 2024 and will cost $125k per “explorer”. Importantly, you can have a beer and relieve yourself while you’re happily floating 100k ft above the rest of us!

SpaceX (private) President Gwynne Shotwell says the company is “shooting for July” for the first orbital launch of Starship, despite not having received the prerequisite approvals. SpaceX has conducted multiple short test flights over the past year with the targeted orbital launch seeing the 55m high Starship boosted into orbit atop the reusable 63m Super Heavy booster.

Other Developments

Shopify (SHOP) had its developer conference this week (Shopify Unite) where they made a number of key announcements. Firstly, the company has amended how they clip the ticket on Shopify App Store revenue. Previously they took a 20% slice of every dollar developers made but now they’ll drop this to zero (for those generating less than $1m) and come down to 15% for anyone over that threshold. Other updates include an upgrade to the Storefronts platform (Online Store 2.0), improvements to Storefronts API and a suite of new features to create a more seamless checkout experience (i.e. Payments Platform to integrate with third-party payment gateways).

Facebook (FB) has released a substack competitor called Bulletin which is in beta launch with a curated list of writers including Malcolm Gladwell, Mitch Abom (“Tuesdays with Morrie”), sportscaster Erin Andrews and fashion designer Tan France. This follows Twitter’s expansion into the newsletter business (Revue) and follows an ongoing theme to maintain product parity - just as we’ve seen with live audio (Clubhouse) and short-form video (TikTok).

On the topic of product parity, the week also saw Slack (soon to be part of Salesforce) announce a bunch of new features such as Slack Huddles which will allow team members to have a live audio chat with their colleagues instead of back-and-forth text (just like real life!). The company is also exploring video message capabilities which would be like an Instagram story, but for work.

Epic Games’ (private) Fortnite has thrown a virtual concert at O2 London Arena in collaboration with O2 and Island Records (owned by Universal Music). The 20 minute event (below) sees gamers ushered through a bunch of surreal worlds listening to the British band Easy Life. It’s all a bit odd but, as we’re seeing with Roblox (RBLX), shows how certain brands are shifting to engage audiences in more innovative ways.

A few quick updates on crypto for the week:

The founders of South Africa’s largest crypto exchange, Africrypt, have vanished, taking with them an estimated $3.6b in Bitcoin. Back in April, the founders alerted clients that they had been hacked but asked them not to alert police or lawyers as it would impede on the recovery of their assets!

Binance is now banned in the UK, with the Financial Conduct Authority (FCA) saying Binance “must not, without the prior written consent of the FCA, carry out any regulated activities...with immediate effect”. This follows further crackdowns in Japan where regulators there claim the company is operating illegally.

Meanwhile, Coinbase (COIN) has received permission from Germany’s BaFin to provide crypto custody services and prop trading, the first such license it has issued in the country. The company also announced that they want to list every crypto asset that is legally possible, whilst working on tools to allow ratings and reviews of such assets (will economic value now be premised on reviews?)

Finally, in order to boost uptake, El Salvador is giving citizens $30 in bitcoin for registering with the sovereign digital wallet “Chivo” ahead of the currency becoming legal tender in September.

SiFive (private) is partnering with Intel (INTC) after releasing a new chip design aimed at challenging the dominance of Arm (private), which itself is in the midst of a takeover from Nvidia (NVDA). Under the agreement, SiFive’s P550 design (and related IP) will be licensed to Intel who will reorganise its fab to create its own SiFive P550-based 64-bit 7nm System on a Chip (SoC) - called Horse Creek. This is a lot to absorb in one paragraph but in essence, this means the door is slightly ajar for Intel as they seek to resurrect their fortunes specifically relating to ‘edge’ computing (i.e. phones, smartwatches, laptops) which has been completely swallowed up by Arm’s architecture in recent years.

ioTech (private) has developed a world-first multi-material additive technology that can process almost any material (acrylate, epoxy, silicone, metal, solder etc) at high resolution and high speed. They call this Continuous Laser-Assisted Deposition (CLAD) technology. CLAD will enable mass-manufacturing capabilities across multiple sectors including semiconductor packaging and printed circuit boards (PCB), manufacturing and assembly. That’s particularly beneficial for anchor investors ASM Pacific (522.HK) and Henkel (HEN3.DE).

Panasonic (6752.JP) sold its entire stake in Tesla (TSLA) for an estimated $3.6bn in the past year according to Nikkei Asia. The company has been a major battery supplier to Tesla from day one, with its first investment of 1.4m shares falling around the time of the company’s IPO. Proceeds from the sale will go towards new strategic investments with both organisations continuing to maintain their strong business partnership into the foreseeable future. One of those strategic investments would be Blue Yonder, a supply-chain software that Panasonic is in the process of acquiring for $7.1b. Meanwhile, Chinese battery maker CATL announced an extension of a battery supply deal with Tesla during the week.

Volkswagen (VOW3.DE) will stop selling combustion engines in Europe by 2035 with the move to stop selling the incumbent vehicles coming “somewhat later” for the US and China. The company’s overarching goal is to be carbon neutral by 2050 at the latest. This puts the automaker (who also own Audi, Porsche, Bentley, Lamborghini and Bugatti) in line with other auto manufacturers like Ford, Honda and Volvo in setting ambitious targets for the European market. The week also saw Renault (RNO.PA) aim for a 65% electrification target by 2025 (previously 30%) with a 90% target set for 2030.

This also comes in a week where VW’s Porsche has established a new venture, Cellforce, to build battery cells in collaboration with Customcells. According to Porsche CEO Oliver Blume, the new subsidiary will be “instrumental in driving forward research, development, production and sale of high-performance battery cells” and will be “how we shape the future of the sports car”.

IPOs | SPACs

Warehouse automation company AutoStore (private) is exploring an ~$10bn listing according to reports from Bloomeberg. Back in April Softbank (9984.JP) announced it had acquired a 40% stake in the company which, at the time, had valued the business at $7.7b. AutoStore’s technology (below) is currently powering over 600 sites around the world. As you can see in the image below, the technology sees a series of robots rolling over a giant Rubix cube, with each square comprising a different product (or SKU). For clients like ASDA, Puma and Best Buy this technology greatly accelerates fulfilment time and customer experience. It also appears an ideal takeover target for someone like Shopify (SHOP) where there would be incredible synergy with their evolving business model (particularly relating to fulfilment).

BuzzFeed (private) is merging with SPAC 890 5th Avenue Partners (ENFA) in a deal valued at $1.5b. Upon closing, the company will then acquire “youth entertainment network” Complex Networks (private) for $200m which will put them on target for $654m in revenue for 2022. By 2024 they expect commerce to comprise one-third of their revenue, with millennials acquiring directly through their various brands which also includes Huffpost, Tasty and BuzzFeed News.

Leading language learning app Duolingo (private) has filed to go public via an IPO. The company disclosed revenues for 2020 hit $162m (more than doubling YoY) with gross profit margins lifting to ~72% (from 68% in 1Q20). Impressively, Net Loss remained fairly stable (at around $16m), thanks largely to a relative drop in R&D expenses (now 45% of GP vs 64% last year). Operationally, Daily Active Users (DAUs) popped 57% YoY, with subscription bookings doubling over the period. Importantly, Duolingo shows clear evidence of ongoing innovation, offering AI-based English tests (below) which is pioneering English proficiency for institutions like Yale, Duke and Georgia Tech. This is in addition to the core app as well as events and podcasts. Valuation-wise, if it trades around the same multiple as Coursera (COUR) it will likely carry a price tag of close to $3bn (that’s ~10x fwd P/S).

Didi (private) surged 28% on its market debut, giving the Chinese ride-sharing conglomerate a valuation of ~$86b. Assuming Didi hit $46b ($300b yuan) in revenues in 2022 (which is probable) then it’s not hard to see it doubling in value over the next twelve months (bringing it in-line with Lyft/Uber multiples). But, that’s if everything goes to plan! On the negative side of the ledger are domestic regulations, US-China tensions, the overhang of Uber (with a 13% Didi stake) all paired with profitability/margin stress.

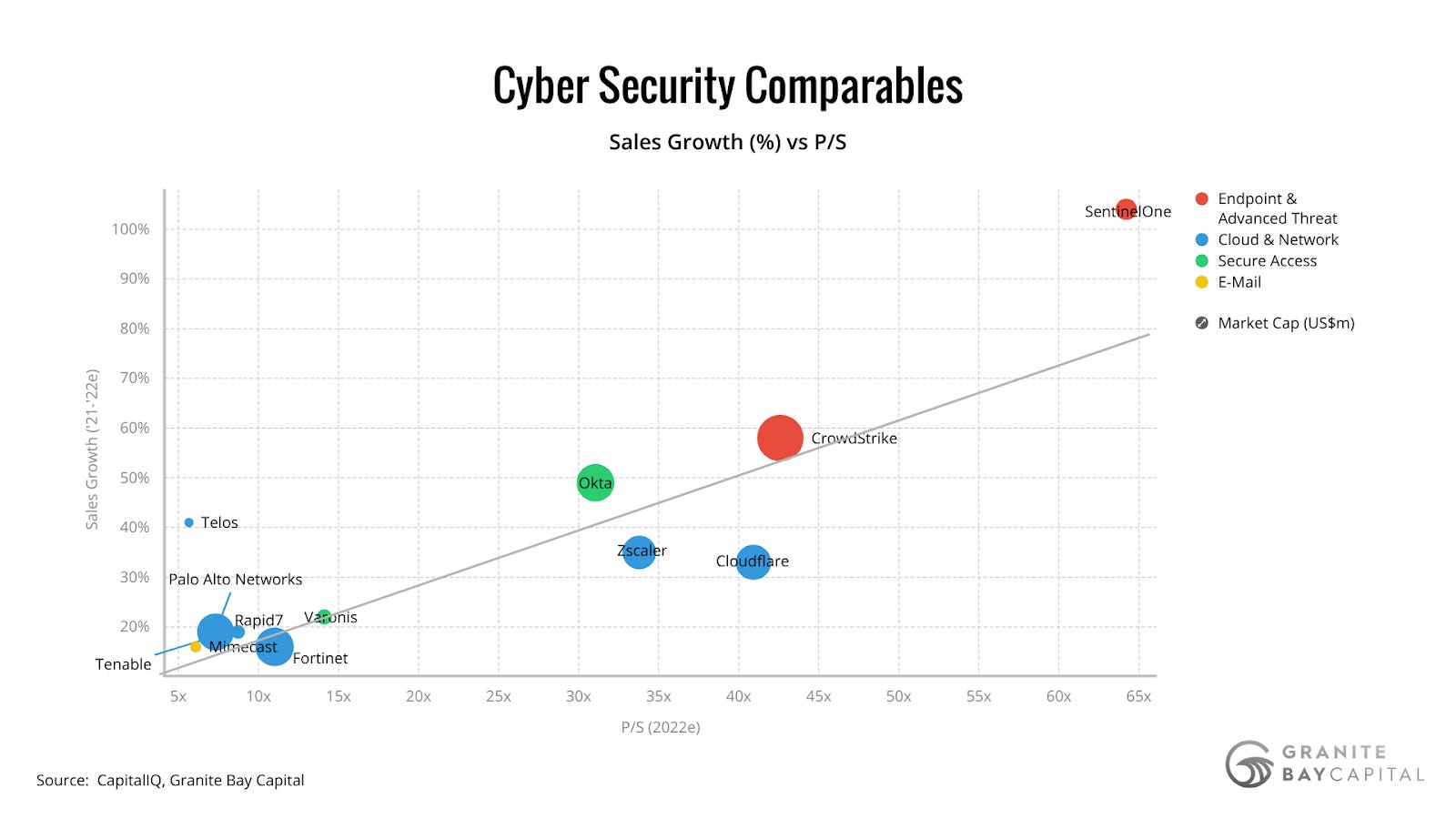

Cyber platform SentinelOne (S) has hit the markets, closing up 21% on day one with a market value of $10.9b. In a nutshell, SentinelOne claims to have built the world’s first purpose-built AI extended detection and response (XDR) that monitors and mitigates cybersecurity threats. So, it’s kind of in the realm of two market favourites - Crowdstrike (CRWD) and Palo Alto Networks (PANW). Valuation-wise, its revenue is doubling YoY, with the market implying a 65x fwd P/S multiple. That’s a lot more than Crowdstrike who, as you can see below, has ~60% sales growth and an implied 43x fwd P/S! Furthermore, SentinelOne’s most recent Gross Profit Margin was 51% vs 74% for Crowdstrike, whilst Operating Expenses for SentinelOne were 4.2x Gross Profit (vs 1.1x for Crowdstrike). So, all in all, SentinelOne needs the financial stars to align to justify its hefty price tag.

Rounding out a lucrative week for debutants, LegalZoom (LZ) closed up 31% as it hit the Nasdaq, valuing the company at $7.35b. The company generated $470m in revenues last year (up 15% YoY) from a range of services including company formation, ongoing compliance, tax advice and filings, trademark filings and estate planning. The company’s aim is to secure customers (businesses) at the point of formation and then lock them in via subscriptions and third-party offerings over the business life.

M&A | Cap Raise | Earnings

Nike (NKE) reported earnings almost 2x analyst estimates, catalysing a 14% rally in the company’s stock. Over the year, revenues increased 19% to $44.5b, with online sales (Nike Direct) surging 73%. According to management, Nike’s ongoing growth will be attributable to three key factors - connecting with consumers through compelling brand experience, driving product innovation (a word mentioned 16 tims in the earnings call) and expanding digital advantage. The image below shows the Nike Go FlyEase - the company’s more innovative “hands-free” shoe.

Visa (V) is acquiring Swedish open banking platform Tink (private) for $2.14b, shortly after it was forced to abandon its offer for US-based Plaid on antitrust concerns. Through the Tink API, over 3,400 banks and 250m customers can access aggregated financial data, use smart financial services and account verification, and build personal finance management tools. Hopefully, this time around Visa can satisfy any regulatory concerns!

Etsy (ETSY) is buying Elo7 (private), the “Etsy of Brazil”, for $217m only a couple of weeks after announcing the $1.6b acquisition of London-based millennial social shopping marketplace Depop (private). The latest deal gives Etsy a footprint in Latin America, where so far they have no meaningful position.

Rockwell Automation (ROK) is acquiring the smart manufacturing platform Plex Systems (private) for $2.22b. For Rockwell, this accelerates their software revenue growth (and ARR streams) through offering customers a more unified connected enterprise platform - one that will now include advanced manufacturing execution systems, quality, and supply chain management capabilities. Meanwhile, Plex peer QAD Inc (QADA) is going private after announcing a $2b offer from PE firm Thomas Bravo (private).

Ionity (private), the EV-charging network co-owned by BMW (BMW.DE), Ford (F), Hyundai (005380.KS), Daimler (DAI.DE) and VW (VOW3.DE), is seeking bids for a 20-25% stake in the business with Royal Dutch Shell (RDS-A) and Renault (RNO.PA) possible contenders, according to Reuters. The company currently has 348 stations across Europe with 45 under construction.

Continuing this week’s space theme, Australia’s Gilmour Space (private) raised $46m from a group of (mostly) local VCs and pension funds as it sets its sights on the launch of its first orbital rocket, Eris, in 2022. Eris will predominantly focus on the launch of nano-satellites into space - a lucrative market but also one that is becoming increasingly competitive from dozens of established and emerging companies respectively, including reusable rockets from Elon Musk’s SpaceX (private), Jeff Bezos’ Blue Origin (private) and New Zealand’s Rocket Lab (private) plus Astra (HOL) China’s OneSpace (private), Northrop Grumman (NOR); and Boeing (B) and Lockheed Martin’s (LMT) United Launch Alliance - to name just a few!

Have a great week.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.