Weekly Innovation Review (WIRE) #39

Latest News from the World's Leading Innovators

Headline Developments

Another week, another major cyber attack! Last Friday, a global ransomware attack hit up to 1,500 companies in what is believed to be the biggest supply chain attack to date. In the attack, American software company Kaseya was compromised, opening a door for hackers to spread ransomware to managed service providers that use it’s technology, and in turn their clients. The attack has been attributed to the Russia-linked REvil cartel which is also suspected to be behind the recent JBS attack. Of course, each attack plays right into the hands of organisations like Crowdstrike (CRWD), Palo Alto Networks (PANW) and recent listings Darktrace (DARK.L) and SentinelOne (S) - and many others (as outlined below).

Richard Branson has confirmed last week’s suspicion, beating Jeff Bezos to space when he boards a test flight of Virgin Galactic on 11th July. Branson will be joined by a crew of six, comprising pilots and space mission specialists - making it the first fully crewed flight for the company. The company will also be live streaming the event which you’ll be able to access here at 6 am Pacific Time on the 11th.

Last week’s good news story is this week’s bad news story! After hitting the markets last week, and rallying 20% on debut, China’s ride-hailing conglomerate Didi (DIDI) has been cited by Chinese regulators for serious violations of laws around the collection and use of personal user data, seeing the stock collapse ~24%. As an immediate consequence, the Government has ordered app stores to remove Didi from their listings, and for the company to stop registering new users. Didi released a statement shortly afterwards indicating that they would be working quickly to resolve the issues. China also cracked down on ‘Uber for trucks’ Full Truck Alliance (YMM) and online recruitment platform Kanzhun (BZ) - both also recent US listings who will be required to halt new user registrations amidst the investigation. Softbank (9984.JP), one of the biggest investors in Didi and Full Truck Alliance, fell 5% following the announcements.

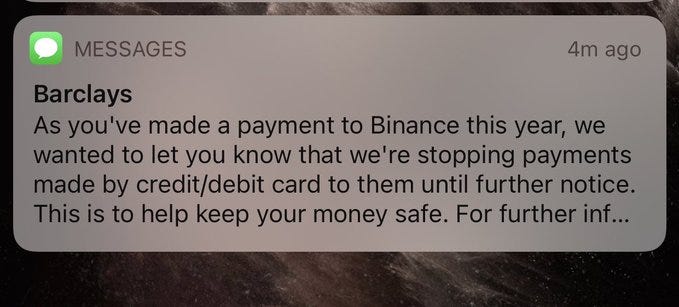

Barclays (BARC.L) is blocking payments to Binance (private) following crackdowns by UK regulators. Other banks such as Monzo and Starling Banks have also reportedly blocked transfers to the organisation as the exchange comes under increased pressure across the globe - Thailand, The Caymans, Singapore, Canada, Japan and the USA. Thailand’s SEC has filed a criminal complaint (here) where they claim Binance has ‘solicited the Thai public’ to use a ‘digital asset exchange without a license’.

Other Developments

NASA is planning to test new solar sail technology in space by the middle of next year. The Advanced Composite Solar Sail System (ACS3) will emerge from a satellite bus, supported by four booms, spanning 9 meters per side. The apparatus works in a similar fashion to sailboats, but instead of using wind, the solar sails “employ the pressure of sunlight for propulsion, eliminating the need for rocket propellant” according to NASA. The technology has been under development since 2018, and in 2020 NASA selected AST Spacemobile’s (ASTS) majority-owned NanoAvionics (private) to build the satellite bus. As an aside, it’s worth your while having a look at the ASTS investor presentation. They listed recently and will be scaling up a space-based cellular broadband network, with the backing of Vodafone (VOD.L), Rakuten (4755.JP), American Tower (AMT) and Samsung (005930.KS); with a whos who of telco customers including Telefonica (TEF), Telstra (TLS.AU) and AT&T (T)

Britain’s OneWeb (private) has sent 36 satellites into orbit on Russia’s Soyuz rocket, paving the way for it to begin rolling out commercial internet services in the northern hemisphere this year. So far OneWeb has 200 satellites in orbit, with aims to have 648 by the end of 2022 (when it aims to have global coverage). OneWeb, bailed out of bankruptcy by Bharti Enterprises (private) and the UK Government in 2020 has gone on to raise additional funding from Softbank (9984.JP), EchoStar’s (SATS) Hughes Network (private) and Eutelsat (ETL.PA). The satellites are manufactured in collaboration with Airbus (AIR.PA).

As you can see below, OneWeb is joined in Low Earth Orbit (LEO) but a whole heap of companies, from the more notable Starlink (private) and Amazon’s (AMZN) Kuiper, through to a growing list of startups from Australia, India, Europe, China and the US. Whatsmore, this rollout of LEO ‘nano’ satellites, will spur a whole suite of new products and services across communications, surveillance, precision agriculture, weather/natural disaster monitoring (to name but a few sectors). The rollout is also being enabled by innovation in rockets, advanced materials and semiconductors; so there are (and will continue to be) immense investment opportunities across the landscape if you know where to look.

Tencent (700.HK) has gone live on facial recognition technology to keep kids off video games! This ties in with a law, passed in 2019, where minors are prevented from indulging in online games - including a ban on minors playing video games from 10 pm to 8 am, as well as limiting their playtime to 90 minutes per day. The same law also prohibits minors from spending more than $57/month on micro-transactions. All individuals (regardless of age) are required to register for games using their real identities and are prohibited from playing anything with “sexual explicitness, goriness, violence and gambling”. Tencent’s new feature, called “Midnight Patrol” scans the faces of players, flagging minors and prohibiting them from playing if they breach any of the regulations. Of course, this data could also be pushed through to the Government as part of its social credit system.

Roblox (RBLX) has signed a deal with Sony (6758.JP) to collaborate on “innovative music experiences for the Roblox community”, offering a range of new commercial opportunities for Sony Music artists to “reach new audiences and generate new revenue streams”. In 2020, Sony artist Lil Nas X “performed” to 36m people in a virtual Roblox concert, including the debut of ‘Holiday’, virtual merchandise sales, mini-games, a scavenger hunt and an exclusive interview.

Future Meat Technologies (private), backed by Archer-Daniels-Midland (ADM) and Tyson Foods (TSN), has opened the world’s first industrial cultured meat facility, with the capability to produce 500kg of lab-grown meat every day. According to the company, this is a critical enabler to bring their products to shelves in 2022. At present, the company produces cultured chicken, pork and lamb. The production process is expected to generate 80% less greenhouse gas emissions, use 99% less land and 96% less freshwater than traditional meat production. Below is a snapshot of some of the major players across cell-based and plant-based proteins. MeaTech (MITC) is one of the few pure-play listed companies in the space, with other exposures indirectly via Tyson Foods and ADM who are active investors in the space (whilst internally developing their own ‘clean’ products).

Rimac (private), the Croatian electric sports car manufacturer, is merging with Volkswagen’s (VOW3.DE) Bugatti. Under the terms of the agreement, Bugatti Rimac (the newco), will be 55% owned by Rimac and 45% owned by VW unit Porsche (who currently own 24% in Rimac). Rimac’s $2.44m Nevara (below) has a top speed of 412km/h and can do 0-100km/h in 1.97 seconds - making it the fastest-accelerating production car in the world! Range-wise it’s expected to do ~650km on a single charge (which, if true, would leave the competition way behind). Obviously, at $2.44m it’s well beyond reach for most consumers, but the technology does show the potential for EV-tech across the entire landscape.

IPOs | SPACs

Robinhood (HOOD) have published their prospectus showing a highly engaged 17.7m MAUs (of 18m net cumulative funded accounts) with $81b in Assets Under Custody (AUC) - 80% equity, 14% crypto. That’s ~$4.5k/funded account, 70% higher than the same time last year. Staggeringly, revenues jumped from $171m in 2019 to $720m in 2020, whilst the company swung from a $106m loss to a $7.5m profit over the same period. However, for the latest quarter, the company highlighted a $1.4b loss on $522m in revenue. The reason for this goes back to Gamestop! At the peak of the meme-stock’s popularity, Robinhood saw surging (often leveraged) volume in stocks. In the two days between trade and settlement, the broker must send cash to the Depository Trust Company as collateral. The issue was - volume was so high that Robinhood had to go back to investors asking for a $3bn loan to cover the collateral. This loan was given (via convertible debt), and it’s translated into a $1.5b accounting blip for the quarter. Separately, CBS reported that Robinhood clients are 14x more likely to default than users of other platforms (like eTrade, TD Ameritrade and others). So, all is fine now, but when the music stops these users are left highly leveraged and vulnerable. It’s up to regulators to enforce some sense of responsibility in these exchanges.

Satellite operator Planet (private), which operates over 200 earth observation satellites, is merging with dMY Technology IV (DMYQ) in a deal valuing the business at $2.8b. According to the company’s investor presentation, they are the leading provider of daily, global earth data (or as they say the ‘Bloomberg’ for Earth Data) with a fleet 10x the competition, generating over $110m in revenues (90% recurring, 110% Net Dollar Retention) from over 600 customers. Customers like Bayer, Google, Syngenta, QBE use the subscription service for a range of purposes such as harvest planning, emergency response, security, forest depletion and asset monitoring. The company is targeting 44% CAGR over the next five years, with gross profit margins expanding from 24% today to 74% in 2026; putting it on a clear trajectory towards being free cash flow positive by 2025.

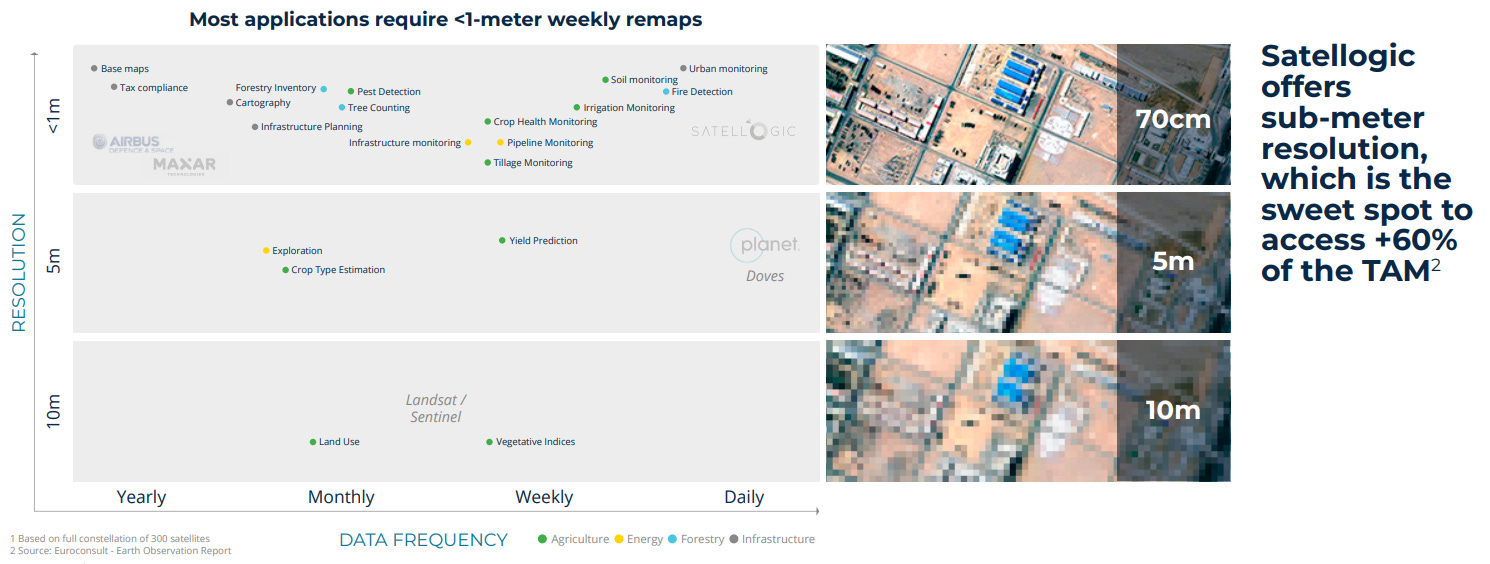

Sattelogic (private), another earth observation startup, is going public via a SPAC, merging with CF Acquisition Corp (CFV). The company currently has 17 satellites in orbit and aims to scale to 300 to provide sub-meter resolution imaging of the Earth updated on a daily frequency. Below is a diagram from the investor presentation showing where they sit on a frequency v resolution basis vs peers.

Swiss conglomerate ABB (ABB) is planning a separate listing of it’s e-mobility division next year, targeting a valuation of ~$3b. The division predominantly makes fast chargers for electric vehicles. It hires 850 staff and posted revenues of $220m last year, averaging annual growth of 50% p/a over the past five years. On that run-rate it will see >$440m in sales next year, implying 7x 2022e P/S. Comparatively, Chargepoint (CHPT) and Blink Charging (BLNK) are trading at 48x and 61x fwd P/S respectively!

M&A | Cap Raise | Earnings

Revolut (private), one of the world’s most innovative banks, is reported to be in talks with Softbank on a $750m-$1bn fundraise that could value the business at over $30bn. Revolut, which has raised $905m since its founding in 2015, offers a range of services across both personal and business banking and has set a benchmark for UX and product innovation across the industry. The company offers services to over 15m personal customers and 500k business customers in over 35 countries around the world. The company saw revenues rise 57% YoY last year to ~$360m. It’s closest (listed) peer is SoFi (SOFI) which, per estimates, is expected to 3x revenues from $565m in 2020 to ~$1.5b in 2022.

Israeli facial recognition startup AnyVision (private) has raised $235m from Softbank, Bosch and Qualcomm as it continues its push into a range of sectors including property, gaming, healthcare, manufacturing and infrastructure. The company’s core platform can be integrated with any camera with 0.1% false alarm and 0.2ms detection speeds, with additional products including touchless access control. However, it’s not without controversy. In 2019 NBC claimed AnyVision was (is) used by the Israeli military to conduct mass surveillance of Palestinians living in the West Bank with one system setup “deep inside the West Bank that try to spot and monitor potential Palestinian assailants''. If this sounds familiar, it is. Various reports have also highlighted Chinese companies Huawei and Macquarie-backed Megvii develop facial recognition technology used to detect Muslim minority groups.

Zipline (private), a/the leading drone delivery startup, has raised $250m in new funding from a group of investors including Temasek, Fidelity and Katalyst Ventures, bringing it to $483m in total funds raised to date and valuing the company at $2.75b. Zipline has built the entire stack of their service (drones, software, launch and landing systems) with partnerships in place with UPS, Walmart and Toyota to deliver everything from medical equipment, personal protective gear, health and wellness products. The drones are catapulted into the air for the delivery and, on return, are caught by a flywire in the air (kind of similar to arresting wires on an aircraft carrier).

Zebra Technologies (ZBRA) is buying warehouse robotics firm Fetch Robotics (private) for $290m after initially buying 5% of the company during its Series C round in 2019. This comes as interest in robotics (particularly industrial automation) is starting to take off. For example, Berkshire Gray is merging with SPAC Revolution Acceleration (RAAC), Autostore (private) is eyeing an IPO and Hyundai have recently closed their acquisition of Boston Dynamics.

The UK’s largest chip producer, Newport Wafer Lab (private), is being acquired by Nexperia - a Dutch chip firm owned by China’s Wingtech. The deal is expected to be valued at ~$87m, however, closure may still be dependent on approval under the National Security and Investment Act. According to Tom Tugendhat, leader of the U.K. government’s China Research Group, the government is “yet to explain why we are turning a blind eye to Britain’s largest semiconductor foundry falling into the hands of an entity from a country that has a track record of using technology to create geopolitical leverage”.

Atotech (ATC), a leading developer of chemicals and equipment for the semiconductor industry, is being acquired by MKS Instruments (MKSI) for $5.1b (roughly half MKS’ current equity value!). The deal is expected to be earnings accretive and additive to free cash flow in year one. According to Atotech’s CEO Geoff Wild “The combination of Atotech’s expertise in electroplating and chemistry and MKS’ strengths in lasers, laser systems, optics and motion will enable innovative and ground-breaking solutions for customers in the areas of materials processing and complex applications”.

Have a great week.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.