Weekly Innovation Review (WIRE) #4

Latest News from the World's Leading Innovators

It seems everyone reported earnings this week! Most of these are highlighted at the end of this week’s review, however, in a nutshell, Pinterest surprise massively (lots of people at home designing post-covid kitchens it seems), Alphabet, Amazon and Shopify hit it out of the ballpark, Apple took a huge hit in China and SAP showed they’re going to struggle to shake the laggard tag, collapsing 30% this week! Goodbye SAP?

Headline Developments

Pinterest (PINS) revenue was up 58% YoY for 3Q20, with similar growth expected for Q420! International Monthly Active Users (MAUs) hit 343 million (up 46%) off a measly 21c average revenue per user (ARPU). By comparison, there are 98 million US users on $3.85 in ARPU. This shows significant potential for ongoing international monetisation. In May, we discussed Pinterest’s transformation journey, with particular interest on the APRU potential from advertising and e-commerce leveraging a very unique user-base (80% of 18-64 y/o mums in the US have a Pinterest account!).

Shopify (SHOP) revenue was up staggering 96% YoY with earnings of $133 million for the quarter. The company also began rolling out its buy-now-pay-later product, Shop Pay Installments and continued to expand the Shopify Fulfillment Network - a network of fulfilment centres seamlessly integrated with a customer’s online store. The chart below from Spotify’s earnings really highlights how much 2020 has accelerated the adoption of e-commerce!

Ant Group (6688.HK) will start trading on 5th November at CNY68.8 (in Shanghai) and HK$80 (HK); raising a total of US$34.5 billion. On this basis, Ant would be worth ~$313 billion. This is bigger than PayPal ($235 billion) and 1.5x bigger than Australia’s top four banks combined! Valuation-wise the IPO price puts it at ~31x 2021e P/E (PayPal 43x, Square 145x) and EV/EBITDA of 24x 2021e (PayPal ~31x, Square 112x)!

The US Government, in a filing with the US District Court, said that the Government should be allowed to impose restrictions on TikTok (private) which will make it unusable in the US next month. An executive order signed by Trump in August bars any US transactions with TikTok’s Chinese parent company ByteDance.

In more positive news for TikTok, they announced a partnership with Shopify on social commerce. The global partnership allows Shopify’s over 1 million merchants to reach TikTok’s user base, initially via optimised ad content, but inevitably through in-app shopping features currently adopted by Instagram and Pinterest (PINS). This isn’t as good for US-based merchants if Trump’s executive order remains!

Facebook (FB) is rolling out its own cloud gaming service. But unlike Google Stadia and Amazon’s Luna, who are offering paid subscriptions for high-quality gaming, Facebook will launch a few titles (i.e. golf, racing) for free within its existing app. According to Facebook’s VP of Play, Jason Rubin, the reason FB is exploring the cloud is that it opens up the types of games it can offer. The platform has been rolled out in beta cross Android.

Fresh on the heels of confirming it’s Xilinx (XLNX) acquisition, Advanced Micro Devices (AMD) launched its latest GPU during the week - three Radeon RX 6000’s (below). According to data shared by AMD, their new GPU performs better (in terms of frames per second) than NVIDIA’s RTX 3080 across a range of titles including Call of Duty and Battlefield V, with less power draw (300w v 320w).

Other Developments

Samsung (005930.KS) and Stanford University have developed a new architecture for OLED that could enable resolutions of up to 10,000 pixels per inch (PPI). Today’s smartphones have around 500 PPI! This is particularly important in the advancement of augmented and virtual reality, where the image is displayed centimetres from the eyes. An illustration of the meta-OLED display is below (source: Stanford).

India’s Future Retail (FRETAIL.NS) have told Singapore arbitrators that they would go into liquidation if the sale of retail assets to Reliance Industries fail. In 2019, Amazon signed a deal with Future Retail to buy 49% of Future Coupons (who in turn own 7.3% of Future Retail). As part of that agreement, Future Retail has restrictions not to sell to “specific persons” (including Reliance), and Amazon also has a right of first refusal to purchase more shares in Future Retail.

Court filings show that Softbank’s (9984.JP) Mayoshi-Son tasked executives to “use whatever excuse” to delay a $3 billion tender offer for shares in WeWork (private), according to Reuters. A transcript submitted as part of a Delaware court filing, shows a message from Son, to WeWork’s Executive Chairman Marcelo Claure, saying “it’s great to postpone the close of tender…...user whatever excuse to make sense”, with Claure responding “Ok. Will use antitrust. I am turning good at excuses like someone I know very well :)”

Dropbox (DBX) will start shifting their storage to Western Digital’s (WDC) Shingled Magnetic Recording (SMR) hard disks. Back in 2017, Dropbox decided to shift away from AWS to their own infrastructure and this step, to SMR, allows them to do that more efficiently. Western Digital says that SMR delivers cost saving through increased storage density and lower power requirements.

Visa (V) is facing scrutiny from the Justice Department’s antitrust division over its $5.3 billion acquisition of Plaid (private). Plaid allows consumers to share their financial information with thousands of apps such as Acorns, Transferwisre, Coinbase and Venmo. Their suits of APIs allow developers to extract data such as transaction history, account balances, user identity and investments.

Harley-Davidson (HOG) revealed the Serial 1 bicycle this week (as opposed to a motorbike!). The electric bicycle is a first for Harley and, based on patent filings, provides a great testing ground for virtual braking, clutch and electrification technologies (on top of existing patents on gyroscopic bike stabilisation) which we feel is highly applicable to future iterations of their LiveWire electric motorbike. Harley has been heavily focussed on innovation of late, to combat an ageing customer-base, attract a younger demographic and provide some confidence to shareholders that their declining earnings can show signs of recovery!

Every week, the space and satellite sector gains more traction.

SpaceX (private) have beta launched their ‘better than nothing’ Starlink satellite service at a cost of $99 per month (plus a $499 fixed cost for the infrastructure). The company expects to see 50-150 Mbps data speeds and latency of 20-40ms over the next ‘several months’ as more satellites and ground stations are rolled out. They expect latency to drop to around 16ms by mid-2021. Competition is getting intense, with Amazon’s Kuiper making very steady progress along with Boeing, Thales, Telesat and, via a partnership model, Microsoft.

Rocket Labs (private), backed by Australia’s Future Fund and Khosla Ventures, launched its fifteenth payload this week, this time carrying one Canon Electronics (7739.JP) satellite (CE-SAT-IIB) and nine Planet Lab’s (private) Flock 4e’ SuperDoves. Both satellites will be used for earth imaging purposes.

While SpaceX, Amazon and myriad other contenders fight for satellite supremacy, a little closer to earth, Alphabet is making their own steady progress.

Alphabet’s (GOOG) Loon, aiming to build out a global stratospheric communications network, set a record this week with one of its balloons spending 312 days in the stratosphere - breaking its prior 223-day record. The company are partnering with the likes of AT&T (T), Orange’s (ORAN) Telkom Kenya, Loral’s (LORL) Telesat, Vodafone’s (VOD) Vodacom and the High Altitude Platform Station (HAPS) Alliance whose ‘executive members’ include AT&T, Airbus (AIR.PA), Intelsat (IJSA.F), Loon and Nokia (NOK).

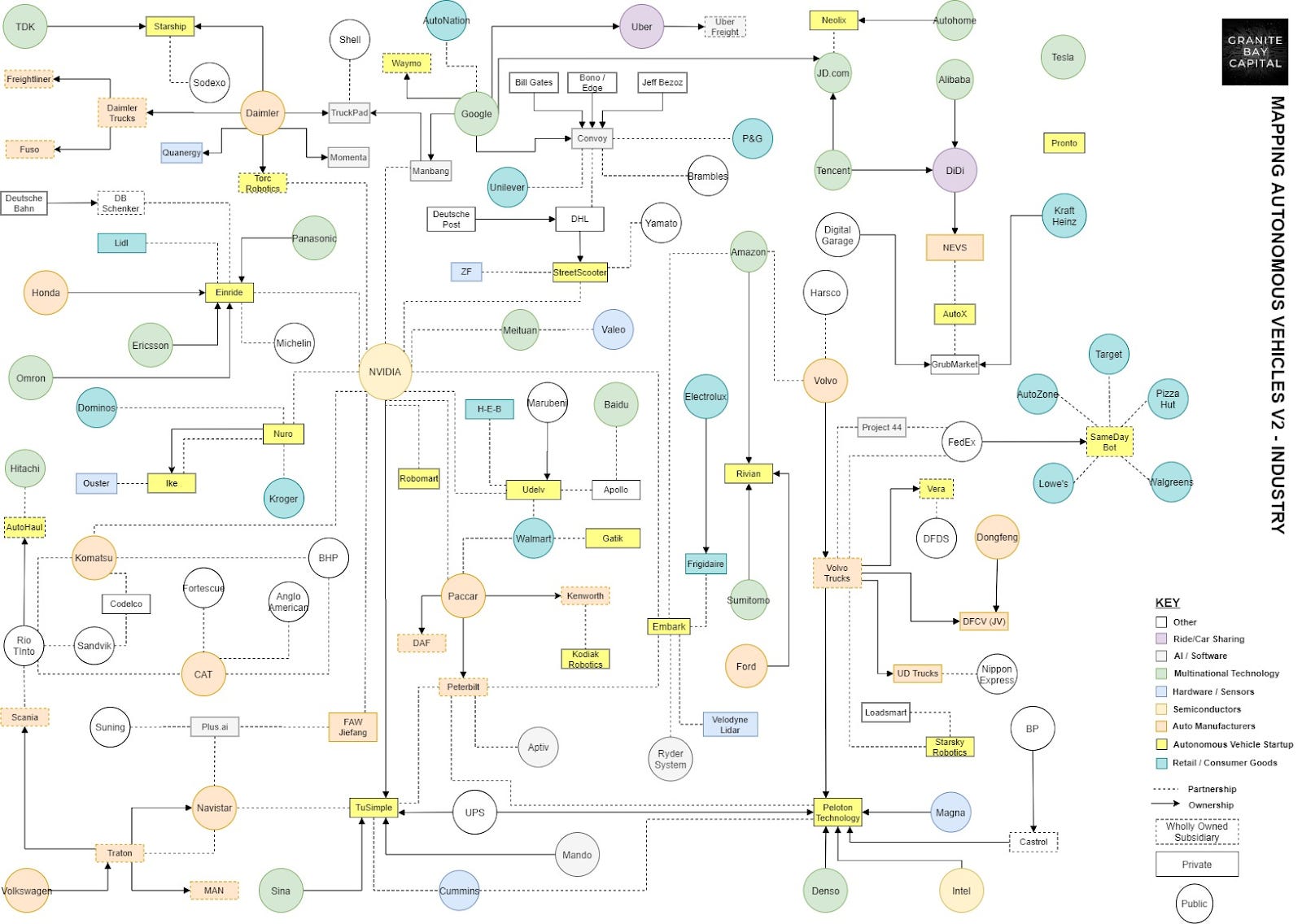

A little closer to earth, Alphabet’s (GOOG) Waymo and Daimler (DAI.DE) announced a “broad, global, strategic partnership” to deploy fully driverless trucks. You can see below (top left), that Damiler are highly active in the autonomous space, with investments / ownership in TruckPad, Momenta, Torc Robotics, Quanergy and Starship and, the Waymo deals helps to unify all of these learnings/investments through, arguably, the most advanced autonomous vehicle platform. Other leaders include TuSimple (backed by Nvidia, UPS, Sina and Mando) as well as the cabin-less Einride, Ike and Kodiak Robotics.

M&A

Advanced Micro Devices (AMD) confirmed the rumours, signing an all-stock deal to acquire Xilnix (XLNC). The deal is valued at $35 billion and equates to 1.7234x AMD per XLNX. According to AMD, the acquisition will be immediately accretive to AMD margins, EPS and free cash flow. At deal close, the combined company will be 74 per cent owned by ADM and 26 per cent owned by XLNX shareholders.

Hot on the heels of AMD, Marvell (MRVL) said it would acquire rival semiconductor firm Inphi (IPHI) for $10bn in cash and stock. Combining Marvell's ($26 billion market cap) storage, networking, processor, and security portfolio, with Inphi's leading electro-optics interconnect platform, will position the combined company for end-to-end technology leadership in hyper-scale cloud data centers and 5G wireless infrastructure.

Earnings

We warned you that it’s a big earnings season this week!

Activision Blizzard (ATVI) earnings were ahead of expectations (more than doubling YoY) on a surge in usage of titles like Call of Duty, Tony Hawk and Crash Bandicoot. Overall the company had 111 million monthly active users (MAUs), led by 80 million downloads of Call of Duty: Warzone.

Alphabet (GOOG) showed a huge bounceback this quarter, with earnings coming in 44% above expectations. Actually, across the board, they beat expectations - revenue hit $38 billion with cloud and YouTube contribution of $3.44 billion and $5.04 billion respectively.

Amazon (AMZN) results beat estimates easily with revenue of $96.1bn (vs $92.7bn expected), and EPS was 67% higher than expected, at $12.37. What was incredible is that Amazon has created over 400K jobs this year! AWS revenue grew 29% to $11.6bn in Q3 and is on track to be a $50bn revenue run rate business!

Apple (AAPL) couldn’t quite match the upbeat earnings season with sales largely inline ($64.7 billion). iPhone sales dropped 21% (as people hold off for iPhone 12), Mac and iPad sales jumped 29% and 46% respectively (on increased remote work) and ‘home and accessories’ jumped 21% for the period. This slight shine was dulled by a whopping 29% fall in China sales!

eBay(EBAY) earnings were ~10% above forecast with 340,000 sellers migrating over to Ebay’s managed payments infrastructure (eBay processed >20% of volume through managed payments in Q3). Meanwhile, Etsy (ETSY) delivered a similar (12%) earnings beat. Etsy and eBay have respectively tripled and doubled in value in 2020 (if you are an e-commerce company and your shares haven’t doubled since March, clearly you are doing something wrong!).

Facebook’s (FB) 3Q revenue hit $21.5bn vs $19.8bn estimates.EPS was 40% higher than estimates. Daily Active Users (DAUs) reached 1.82 billion (from 1.62 billion in 3Q19), with little help from the US and Europe which saw zero user growth. Global ARPU hit $7.89 ($39.63 for US/Canada, $12.41 for Europe, $3.67 for Asia and $2.22 for RoW). As a reminder roughly ¼ of the world uses Facebook daily!

Fastly (FSLY) reported revenue of $70.6 million, up 41.9% YoY. However, the stock is down 50% this month for several reasons - primarily because its largest customer (TikTok) migrated traffic from Fastly due to regulatory concerns and secondly, because several existing customers expected to ramp traffic in late Q3 didn't ramp until early Q4, creating a timing issue.

First Solar’s (FSLR) posted a 70% increase in sales during the quarter, allowing it to reinstate full-year guidance (previously withdrawn due to COVID-19). FSLR expects revenue of $US2.6-2.9 billion for 2020, as its productive capacity has been averaging over 100% at all of its factories.

Microsoft (MSFT) reported 1Q21 revenue came in at $37.2 billion (v $35.7 billion forecast). Azure revenue (not disclosed) was up 48 per cent whilst Teams rode a surge in demand, reaching 115 million Daily Active Users (DAUs) v 75 million in April!

Samsung Electronics (005930.KS) reported a 59% jump in operating profit for Q3, however, they expect 4Q profit to fall due to weak server chip demand and rising smartphone competition. The company’s chip profit surged 82% (largely due to an inventory buildup from Huawei ahead of US-restrictions).

SAP(SAP) collapsed over 20% following a poor outlook for the year. Their co-founder and Chairman, Hasso Plattner, subsequently bought ~$300m worth of stock (he owns ~6%). Salesforce CEO Marc Benioff criticized SAP saying “They have not executed the cloud opportunity well,” and that “SAP’s troubles, I think, are unique to them.” We tend to agree with Marc.

Twilio (TWLO) reported better than expected results this week with revenue up 52% to $449m (vs consensus of $410m). Active customers grew to 208k (vs 172k in 3Q19) and, impressively, Net Dollar Retention increased to 137% (vs 132% in 2Q20).

Twitter (TWTR) revenue was up 14% YoY to $936 million, however, they added just 1 million DAUs versus the previous quarter (now 187 million). The stock is down 15% in the aftermarket post result.

2U (TWOU) the online education provider grew revenue 30.7% to $201.1m in 3Q20. COVID-19 has accelerated demand across all three primary products — short courses, boot camps and degrees.

We promise next week, with fewer earnings to report, that the weekly review will be a tad shorter!!

Have a great weekend.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.