Weekly Innovation Review (WIRE) #42

Latest News from the World's Leading Innovators

Headline Developments

Another bad week for Didi (DIDI), with the stock plummeting a further 21% after Bloomberg reported that Chinese regulators were weighing up “serious, perhaps unprecedented penalties” which may include a hefty fine (>$2.8b), enforcing a state-owned investment or delisting the company from the NYSE. This stems from two investigations into Didi, one around anti-competitive practises and a second relating to the safeguarding of national data. The investigations have led to a 50% sell-off since the company was listed just a few weeks ago. Separately, Tencent (700.HK) are getting on the front foot, temporarily suspending new user registrations for subsidiary WeChat as it works to upgrade its security technology to align with relevant laws and regulations.

Fresh from his space soiree, Jeff Bezos is throwing an extra $2bn at NASA to cover some of their costs and put Blue Moon (below) back in contention to be part of the moon’s Human Landing System (HLS). Due to a funding shortfall, this contract was awarded solely to SpaceX back in April, after NASA had initially indicated they were looking to contract multiple companies. In a letter to NASA’s administrator Bill Nelson, Bezos wrote “Blue Origin will bridge the HLS budgetary funding shortfall by waiving all payments in the current and next two government fiscal years up to $2bn to get the programme back on track right now”, adding that “this offer is not a deferral, but is an outright and permanent waiver of those payments”.

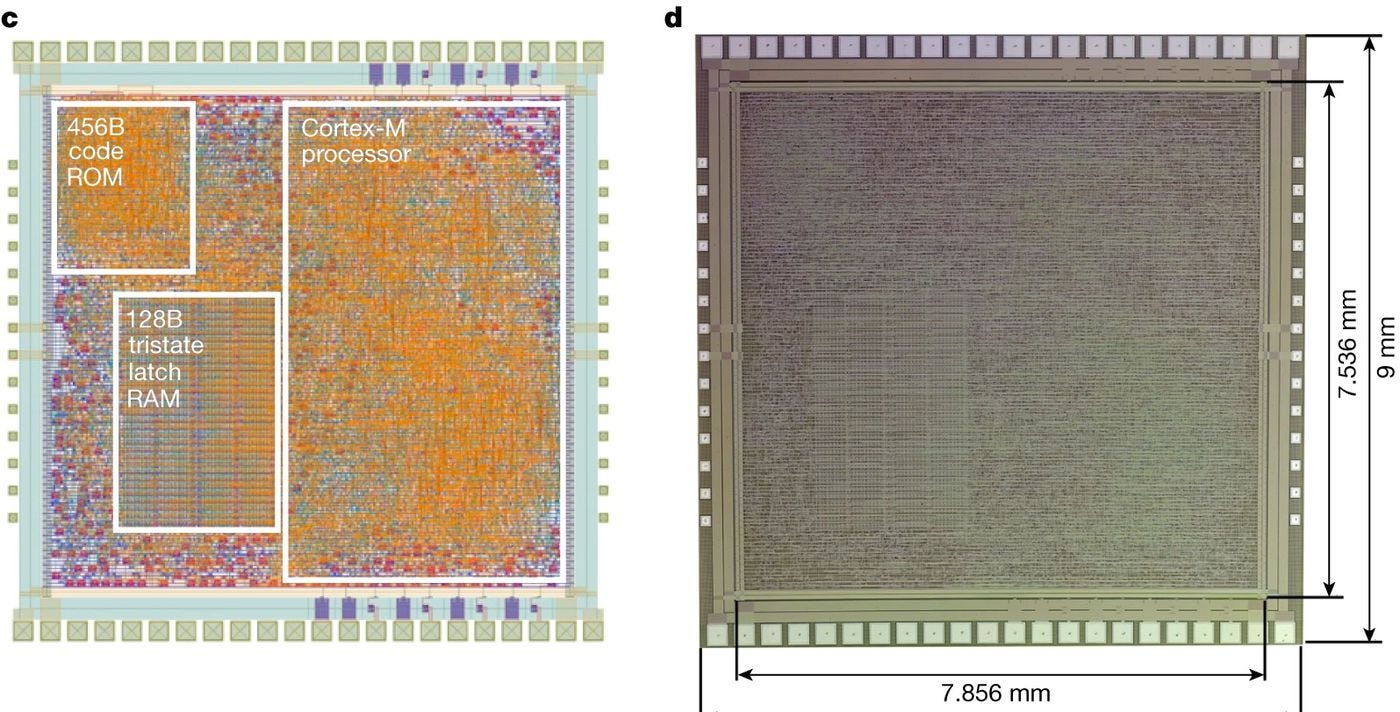

A big leap for ubiquitous computing this week, with Nvidia (NVDA) target and semiconductor pioneer Arm Holdings (private) unveiling a fully-functional prototype plastic-based microchip called PlasticARM (below), enabling semiconductors to be applied to malleable surfaces like paper and plastic. This is primarily enabled due to metal-oxide thin-film transistors (TFTs) which can bend and flex without degrading. The chips are nowhere near as efficient or powerful as what you’ll see in a typical edge device (i.e. Apple watch) but it does open the door for some incredible innovations, like smart tags to detect food spoilage and smart clothing. For a glimpse of how this may look, check out this clip from Wiliot, an Amazon / Qualcomm / PepsiCo backed startup developing similar flexible smart tags (discussed more in the cap raise section below).

Other Developments

Facebook (FB) is creating a product team to work on the metaverse - a virtual shared space that is currently being led by gaming companies like Roblox (RBLX) and Fortnite (private). According to Andrew Bosworth, the head of Facebook’s Reality Labs, “Portal and Oculus can teleport you into a room with another person, regardless of physical distance, or to new virtual worlds and experiences….but to achieve our full vision of the Metaverse, we also need to build the connective tissue between these spaces”. It’s Mark Zuckerberg’s vision that over “the next five years or so” people start seeing Facebook as less of a social media company and more of a Metaverse company. The announcement from Facebook isn’t a huge surprise given the development of VR game Horizon and the recent acquisition of collaborative game creation platform Crayta (below) which will play a big part in the development of this metaverse “connective tissue”.

Daimler (DAI.DE) unit Mercedes Benz is throwing $47b at electrification of its lineup as it announces plans to go all-electric by 2030. The caveat here is that they’ll only go all-electric in markets (like Europe and North America) “where conditions allow”. According to Daimler Chairman and head of Mercedes-Benz Ola Kallenius “we are convinced we can do it with strong profitability, and we believe that focus on electrica is the right way to build a successful future and to enhance the value of Mercedes Benz”. The flagship EQS (below) has a whopping 767kms of range, getting 300kms charge in 15mins and, according to CNET’s first drive review is a “big effing deal” that “sets a new high-water mark for high-dollar electric vehicles”.

Intel (INTC) have outlined their processor roadmap for the next five years at the Intel Accelerated webcast. In this, the company has ‘refreshed’ the naming of their processors. So the nextgen 10nm process will be called Intel 7 (release 4Q21), 7nm will be Intel 4 (due 2023), the amped-up 7nm (18% better performance/watt v Intel 4) will be called Intel 3, and any developments beyond 7nm are effectively called 20A and 18A (the ‘A’ being a reference to Angstrom - a unit of measurement smaller than a nanometer). To achieve this greater efficiency Intel will be relying on a new transistor architecture called RibbonFET, which effectively creates greater chip density (if you want the minute detail read this)!

An added bonus for Intel is that Qualcomm has agreed to come on board to procure chips from this new process. That helps vindicate the chip roadmap and Intel’s fab services strategy (where they’re looking to make chips for other companies and be more competitive with TSM and Samsung). However, a lot needs to go right for this strategy to succeed; and if it does succeed it only really puts Intel on product parity with their competitors (assuming those competitors don’t continue to outpace in terms of innovation).

Scott Snyder, the famed comic book writer behind Batman, Justice League and American Vampire, has inked a deal with Amazon (AMZN) covering seven upcoming comic book series (below). The deal will see the comics appear first on Amazon’s digital comic service ComiXology and Kindle and give Amazon ‘first look’ at film, TV and merchandising (but no strict rights). With Disney owning Marvel and Netflix ramping up its investment in comic adaptations (and animated series), the Snyder deal

Google is graduating robotics software and AI company Intrinsic from its innovation lab “X” - the home of AV company Waymo and internet balloon network Loon (and many more). In a nutshell, Intrinsic aims to make industrial robots (from the likes of Kuka and Yaskawa) more intuitive and easier to use. For example, two robots working collaboratively putting together IKEA furniture.

iRocket (private), a New-York based developer of 3D printed reusable rocket engines and launch vehicles, is entering into a partnership with NASA to help accelerate its commercialisation. Under the deal, iRocket will have access to testing facilities and engineering support at NASA’s Marshall Space Flight Center in Alabama. The first milestone will come in September with a planned engine-firing test for methane-powered rockets that will eventually power the Shockwave launch vehicles. These vehicles are targeting a payload of 300kgs and 1,500kgs.

A gigantic kick in the guts for investors in China’s education space, with new regulations coming in banning companies that teach school curriculum subjects from making profits, raising capital or listing on the stock exchange. The regulations also prohibit the companies from taking foreign investment. As a result, leading edtech companies TAL Education (TAL), New Oriental (EDU) and Gaotu Techedu (GOTU) collapsed ~70% each.

China has unveiled plans to build a ‘clean’ nuclear reactor using thorium and molten salt, with a prototype reactor expected to be ready by August, and a full-scale commercial reactor set up by 2030. As opposed to conventional nuclear reactors, the output of thorium reactors (uranium-233) can be largely recycled with ‘leftovers’ having a half-life of 500 years (vs 10,000 years for conventional nuclear reactors). Furthermore, the tech doesn’t require water, and can’t easily be used to produce nuclear weapons. Ultimately, China aims to build 30 such reactors in countries participating in the belt and road initiative. According to the World Nuclear Association, ~42% of the world’s thorium is in India, Brazil, Australia and the USA.

IPOs | SPACs

Duolingo (DUOL) hit the markets overnight, surging 36% on debut and valuing the company at $5bn. According to the prospectus, the gamified language learning app saw revenue growth of 129% last year (to $161m) with quarterly revenue jumping 97% in the current quarter. The company offers 95 courses across 40 languages, with 40m MAUs and over 500m downloads.

Earnings

This week we’re seeing everyone report quarterly earnings. It’s impossible to report on them all but, to make things easier, I’ve outlined some of the key releases in a graph below, followed by commentary on the stand out performers (or underperformers).

Firstly, in the chart you’ll see revenue beat (y-axis) vs bottom line / EBT beat (x-axis). Of course, a beat on these metrics doesn’t correlate to the market performance of the stock (i.e. the company may revise forecasts, or subscriber growth/margins may be off). This share price reaction is represented by green (outperform), grey (flat) and red (underperform). Notably, Snap (SNAP) is the clear winner - beating forecasts across the board with shareholders pushing the stock up 20%+. Conversely, Logitech (LOGI) outperformed on top and bottom line but was sold off due to lacklustre guidance.

M&A | Cap Raise

A huge deal in the auto industry with Canada’s Magna (MGA), a leading supplier of auto components, merging with Sweden’s Veoneer (VNE); triggering a whopping 56% surge in the latter’s share price. According to Magna’s CEO Swamy Kotagiri “Veoneer’s complementary technology offerings, customer base, and geographic footprint make it an excellent fit with our ADAS [advanced driver assistance systems] business”. The deal, already indicatively approved by 40% of independent shareholders, is expected to deliver $100m in annual synergies by 2024 and generate Pro-forma sales in excess of $1.2b.

Uber (UBER) Freight, the trucking unit which connects truckers with shippers, has purchased the world’s largest managed transportation service provider - Transplace - in a deal worth $2.5b. The Transplace managed transportation and logistics networks has over $11b in Freight Under Management (FUM) and 62,000 unique users, giving customers carrier insights and “access to a vast shipper network that enables flexibility and nimble decision-making to consistently improve” supply chain performance. This is a great deal for Uber as they shift strategy away from moonshot bets in autonomous vehicles / flying cars and into more immediately profitable (and synergistic) deals like this.

UK digital bank Starling (private) has acquired buy-to-let mortgage lender Fleet Mortgages (private) for $69m. This is part of a wider plan for the neobank to expand beyond lending. According to Starling CEO Anne Boden, the acquisition of Fleet’s $2.4b mortgage book is “the start of our move into mortgages as an asset class”. This comes at a time of rapid product development for neobanks (and consumer-facing fintechs in general) as they look at new ways to engage and retain consumers amidst intensified competition - from other neobanks and conglomerate fintechs like PayPal.

Wiliot (private) is worth ~$500m after raising $200m in funding from Softbank, Amazon, Merck, NTT Docomo, Qualcomm, Samsung and Verizon. In a nutshell, Wiliot has developed flexible chips the size and thinness of a postage stamp that comprises RAM, ROM, sensors, Bluetooth, an ARM CPU, memory and secure communications. Effectively a flexible SoC like what ARM is now rolling out in the headline story. The aim is for tens/hundreds of millions of these chips to be embedded across FMCG, pharmaceuticals, fashion, furniture to provide feedback on freshness, temperature, stocktake, provenance….you name it.

EV startup Rivian (private) has just completed a $2.5b cap raise, backed by existing investors Amazon (AMZN) and Ford (F). The two companies are collaborating with Rivian on respective delivery vans and passenger vehicles with each owning over 10% in the startup. In further news, Rivian is seeking a location for its second manufacturing facility (which will also produce battery cells), with a number of US states reported to be lining up.

Have a great week.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.