Weekly Innovation Review (WIRE) #44

Latest News from the World's Leading Innovators

Headline Developments

On the back of the Epic v Apple case, documents were released highlighting that Google (GOOG) had considered buying Epic outright. During the case, Epic Games outlined Google’s plans to develop “a series of internal projects to address the ‘contagion’ it perceived from efforts by Epic and others to offer consumers and developers competitive alternatives and has even contemplated buying some or all of Epic to squelch this threat”.

With that in mind, we learned this week that a trio of senators in the US has introduced a bill to rein in app stores of companies they said exert too much market control. In essence, the bill’s aim is to bar big app stores (i.e. Apple and Google) from requiring app providers to use their payment system. It would, according to Reuters, also prohibit them from punishing apps that offer different prices or conditions through another app store or payment system. According to Democratic Senator Richard Blumenthal “I found this predatory abuse of Apple and Google so deeply offensive on so many levels”.

China’s regulatory crackdowns continue this week, with prosecutors in Beijing suing Tencent (700.HK) claiming that WeChat’s “youth mode”, which limits certain gaming, social and payment activity, does not comply with laws to protect minors. As an immediate response, Tencent has limited access to its flagship game Honor of Kings, in what is likely to be a small step towards a complete overhaul of how Tencent serves gaming content in China down the line.

As expected, these ongoing regulatory crackdowns are impacting foreign direct investment in China’s tech ecosystem, with one of the world’s largest funds - Softbank’s (9984.JP) Vision Fund - cutting back on new investments in China (which at present account for 23% of its portfolio thanks largely to stakes in Alibaba, Didi and ByteDance).

Now to the biggest decentralised finance (DeFi) hack in history!

Chinese DeFi platform Poly Network has been hacked, with ~$600m in crypto vanishing from the platform. Some of the assets had been initially liquidated, whilst other conversions (like $33m converted via Tether) have been frozen. But here’s where the plot thickens. Following pleas from Poly Network for the funds return, the hacker…..staggeringly…... began returning the funds, with $258m transferred as at the time of writing.

Despite this attack, Reuters has reported that overall crypto crime has dropped sharply to $681m up to July compared to $1.9b in 2020 and $4.5b in 2019 (although DeFi attacks, excluding Poly Networks, continue to hit record highs).

Other Developments

Nvidia (NVDA) has announced that it is launching a major expansion of its Omniverse platform - which is delivering the foundations of the metaverse, digital twin and simulated environment. The expansion sees it integrate with open source 3D animation tool Blender (private) and Adobe (ADBE), opening up to millions more users. The Omniverse platform (below) allows for global collaboration in real-time across various software applications in a shared virtual world. Since launching the open beta platform in December, over 50,000 individual creators and over 500 companies, including Lockheed Martin (LMT), have downloaded and evaluated the platform.

The world’s leading 2D/3D engine Unity Technologies (U) has announced the acquisition of Parsec (private), a remote desktop tool, for $320m. The company, which is effectively a TeamViewer (XTRA.TMV) for creatives, started life as a tool to stream games from high powered computers to generally less powerful devices. The strength of that tool (low latency, high-res support) inevitably made it the ideal tool for game-makers and other GPU-intensive sectors like broadcasting, architecture and post-production.

It’ll be hard to imagine a future where gaming, metaverse, AR/VR, broadcast, design and any other immersive experience isn’t enabled by Nvidia or Unity!

Salesforce (CRM) is getting into the streaming, with 50 editorial leads and hundreds of staff working on the new Salesforce+ product aimed at delivering Dreamforce-type content across four channels - Primetime (news and announcements), Trailblazer (training content), Customer 360 (success stories) and Industry Channels (industry-specific offerings). This isn’t meant to be a Netflix or Disney+ competitor, but rather a logical and innovative evolution of Dreamforce which can now be available year-round to engage existing customers (and acquire new ones!).

Germany’s Delivery Hero (DHER.DE), the owner South America’s PedidosYa, Asia’s foodpanda on top of a dozen other global delivery companies, has picked up a 5% stake in rival Deliveroo (ROO.L), sending shares in the UK-based company up 10%. This is hardly surprising given Delivery Hero’s acquisition spree of late which has included Spain’s Glovo and UAE’s InstaShop (as well as Zomato’s UAE business which they bought for $172m back in 2019). According to Delivery Hero’s CEO Niklas Oestberg (on Twitter), they started buying shares back in April with a firm belief the company was oversold. He mentioned specifically that the implied EV when they bought their stake was £3.6b vs a GTV run-rate of £6.6b and that “in no scenario would this be a bad investment long term”.

PayPal’s (PYPL) personal finance/payments app Venmo is expanding its support for crypto, launching a new feature that will allow users to buy cryptocurrency using the cashback they earned from their Venmo purchases. Cardholders will now be able to purchase Bitcoin, Ethereum, Litecoin and Bitcoin Cash through the new “Cash Back to Crypto” option, rolling out now on the Venmo app. At present, Venmo cardholders earn monthly cashback across eight spending categories such as transportation, travel, grocery, bills and entertainment.

New-Zealand’s Rocket Lab (private) is readying for its first moon launch, aiming to launch the CAPSTONE (Cislunar Autonomous Positioning System Technology Operations and Navigation Experiment) CubeSat towards the end of the year on its Photon platform (below). CAPSTONE is a 25kg satellite created by Advanced Space (private) that will act as a precursor for future moon-orbiting outposts under NASA’s Artemis program. Separately, Rocket Lab has signed a multi-launch agreement to send BlackSky imaging satellites into Low Earth Orbit (LEO).

It was similarly good news for competitor Astra Space (ASTR) this week, surging ~40% following the announcement of its first launch of the year later this month. The launch is the first of two for the U.S. Space Force’s Space Test Program, with the second set for later in the year. Astra claims to have 50 launches in its backlog.

IPOs | SPACs

TikTok parent ByteDance (private) is shrugging off the current regulatory crackdowns, eyeing off a Hong-Kong listing by early next year, according to the FT. Apparently, ByteDance has spent the past few months addressing China’s data security regulations, including how it stores and manages consumer information. ByteDance had eyed off a US-listing but for various reasons (including heightened national security/data privacy concerns in the US and elsewhere) has settled on Hong Kong.

Peer-to-peer car sharing platform Turo (private) has confidentially filed for an IPO. The company has raised ~$470m to date from a list of investors including IAC, Daimler, GM, BMW and Amex. It’s platform is much like an Airbnb for cars, allowing car owners across the globe to rent their vehicles (like the 2021 Chevrolet Corvette available for $333/day in San Diego). Earlier this year, CEO Andre Haddad said the company had generated its first quarterly profit, with full-year profitability earmarked for 2021 (in 2H21 it is targeting $92m in revenue).

Krafton (259960.KS), the South-Korean game developer behind the hugely popular Player Unknown Battlegrounds (PUBG) franchise, hit the markets this week, falling 15% on debut (likely due to concerns over crackdowns in China, which is a major market for the company). This puts it on a market cap of ~$20b, 20% more than Korea’s now number 2 gaming company NCSoft (036570.KS).

Earnings

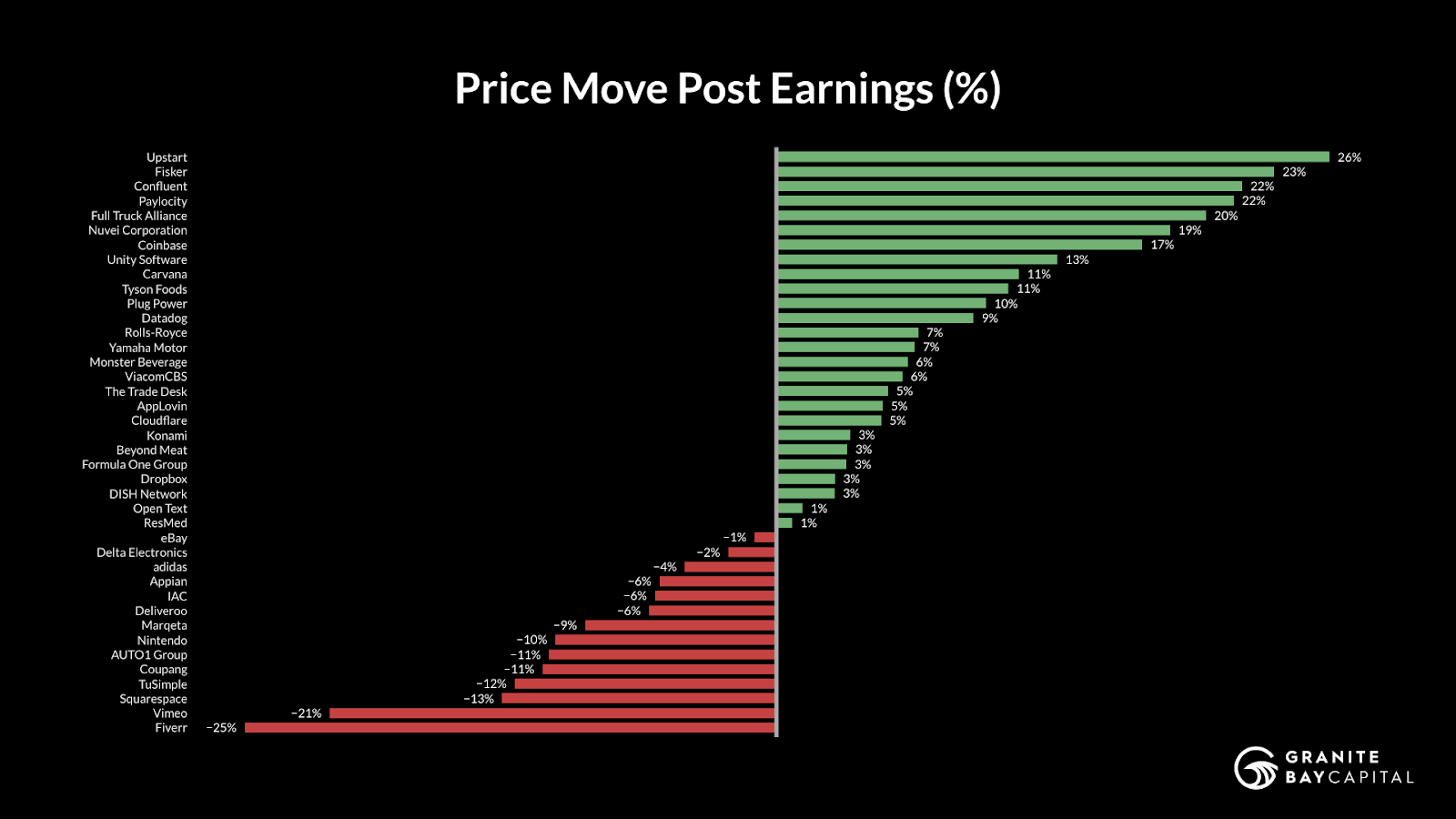

From the below chart, you can see some widely mixed reactions to earnings this week.

Let’s start with some of the major winners:

Upstart (UPST): Revenue climbed 11x YoY to $194m, with 25 banks and credit unions now using the loan platform. In June they hit 100k loans and $1bn in origination volume.

Fisker (FSR): Nothing noteworthy in earnings, but a sizable price move off the back of a bullish Morgan Stanley note saying Fisker may be "one of the only EV-related startups to actually launch on time and ramp up efficaciously in late 2022".

Confluent (CFLT): Topline beat, 13% raise to guidance, 51% YoY growth - all leading to a 20% rally

Coinbase (COIN): Revenue and earnings both surging beyond analyst estimates. Monthly transacting users grew to 8.8m (up 44%).

Unity Technologies (U): Better than expected results, an increase to guidance and positive clarity surrounding advertising spending via the Apple ecosystem.

Carvana (CVNA): First profitable quarter (vs a net loss expected). Revenue tripled YoY. Shortfall in new car production continues to buoy the sector. One of the stronger names in the sector alongside Auto1 (XTRA:AG1) which was off 10% post-earnings (catalysed by a pre-IPO seller)

And the losers (note - a lot of these price moves are decent over-reactions!):

Fiverr (FVRR): Demolished by the market despite beating estimates, raising guidance and signing partnership deals with Salesforce and Wix. Very odd price move.

Vimeo (VMEO): Fell off the back of guidance revision despite strong 43% rev & 58% gross margin growth (and gross margin improvement from 66% to 73%).

Coupang (GPNG): Overall underwhelming numbers for a very hot sector. Big miss on bottom line and revenue was in-line.

Nintendo (7974.JP): Revenue and profit down YoY (after a stellar 2020). Switch sales down 22%, software sales down 10%.

Marqeta (MQ): Very strong results, but still ~90% of revenues coming from 5 customers (namely Square). Despite that, well-positioned through upcoming partnerships (i.e. Google) and central role it plays within the ecosystem.

M&A | Cap Raise

Qualcomm (QCOM) has offered $4.6b ($37/share) to acquire Veoneer (VNE), trumping Magna’s (MGA) $3.8b ($31.25/share) deal by around 18%. As a result, Veoneer has agreed to enter talks with Qualcomm after the board deemed it a “superior offer”. Based on those talks, and in the absence of an increase in terms from Magna, it’s likely Veoneer modified their position to recommend the super offer from Qualcomm - with whom they are actively collaborating, particularly regarding Advanced Driver Assistance Systems (ADAS).

NortonLifeLock (NLOK) is merging with Avast (AVST.L) in a deal worth more than $8bn, and creating a global cybersecurity behemoth available to more than 500m users. According to Norton’s CEO Vincent Pilette, the deal “is a huge step forward for consumer cyber safety” which would lead to “enhanced solutions and services, with improved capabilities”.

Pokemon Go developer Niantic (private) has acquired 3D scanning app Scaniverse (private) which they say will enable more multi-OS scanning easier and enable a more immersive AR experience across its current and future pipeline of AR games. The platform, highlighted below, allows users to capture and edit 3D images of people/objects/places seamlessly with their mobile devices. It’s also highly complementary to Niantic’s prior acquisition of 6D.ai.

Sony (6758.JP) has closed the acquisition of anime streaming site Crunchyroll (private) for $1.175b. According to the latest numbers, Crunchyroll has “120m registered users across more than 200 companies”. By integrating with Sony’s Funimation, the company will have “an unprecedented opportunity to serve anime fans like never before and deliver the anime experience across any platform they choose”.

Esports platform Skillz (SKLZ) has taken a minority stake in Exit Games (private) - developer of the Photon networking engine and platform which enables real-time multiplayer gaming, and used by 580k developers including Ubisoft, Oculus, Square Enix and Bandai Namco….you name it. The deal, which follows the $150m acquisition of mobile marketing platform Aarki in June, will create a huge opportunity for Skills and enable more seamless, low-latency multiplayer experiences and - according to Skillz CEO Andrew Paradise - accelerate their entry into genres like “fighting, first-person shooter, and racing”.

SpaceX (private) is buying Swarm Technologies (private), a leading developer and operator of nano-satellites for IoT applications across the agriculture, maritime and energy industry. At face value it appears an odd deal given SpaceX manufacture their own satellites in-house (or sub-contracts), however, for the undisclosed price, SpaceX is acquiring a highly capable team of ~30 with deep expertise (and IP) beyond SpaceX’s current domain of broadband internet satellites (under Starlink). So far Swarm has deployed 120 of their planned 150 satellites (which fits in the palm of your hand).

John Deere (DE) is acquiring Bear Flag Robotics (private) for $250m, a developer of autonomous technology for tractors. The company, which was only founded in 2017, retrofits existing tractors with a suite of cameras, LiDAR, radar and software, overseen by human supervisors from a personal device (or control room). The startup has been working with John Deere for some time, being part of Deere’s Startup Collaborator program in 2019.

Have a great week.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.