Weekly Innovation Review (WIRE) #56

Latest News from the World's Leading Innovators

Headline Development

A lot of momentum continues around the metaverse.

A few people were close to the pin on Facebook’s new name…..MetaBook, Metanet, MetaRack...even MetaMark being amongst the favourites. However, Meta came out on top - or Meta Platforms (MVRS) to be precise. The name change had a few mixed reactions..the biggest being….what do we now call the FAANG stocks? Well, Mad Money’s Jim Cramer is favouring dropping Netflix from the group and renaming it MAMAA (Meta, Apple, Microsoft, Amazon, Alphabet).

Soon after that name change, Meta Platforms (MVRS) did a bit of “out with the old, and in with the new”. Firstly, they’ve dumped their facial recognition system (the one that automatically identifies friends and family in pictures!) as part of a “company-wide move to limit the use of facial recognition in our products”. This is a quick fix to appease some of the current concerns around facebook’s data capture and privacy.

This news came as Facebook announced a further exemption into VR, with the acquisition of Within - the company behind VR workout app Supernatural (below) which, to date, has only been available on Meta’s Oculus VR platform. With this acquisition, and Facebook’s new direction, it’s quite easy to see how this could kick off a new trend in VR workouts (i.e. imagine doing a HIIT workout in VR with friends from around the world?). All one step closer to reality.

Tinder parent Match Group (MTCH) have launched a new in-app currency, Tinder Coins, which will form part of a broader strategy around the metaverse where you will one day be speed dating with your avatar. This starts with tinder coins, which will reward users today for basic activities like profile completeness, however, in future the plan is to develop virtual goods which can be traded and gifted on the platform (think digital flowers and tiaras). All of this will culminate in something like Single Town, a metaverse experience developed by Hyperconnect (which they acquired for $1.73bn earlier this year). Given you can make an avatar look like anyone, it’s sure to reveal a few surprises for Tinder swipers of the future!

A little closer to reality though is Microsoft (MSFT) who are now bringing their virtual experiences platform, Mesh, under the umbrella of Teams. This means you’ll be able to participate in a Teams meeting as your avatar. From 2022 this will expand to VR, meaning you will walk around the meeting room in VR, engage with co-workers, ideate on the whiteboard etc (it will also auto-translate conversations). These virtual spaces will be built by your organisation within the Teams environment.

Other Developments

Roblox (RBLX) was the latest company to be hit by an outage, going down from the 28th October to 31st October, due to a “subtle bug” as opposed to the more widely speculated cause - a Chipotle free burrito promo, with the chain giving away $1m worth of free burritos to Roblox users. But, while this was bad news for Roblox, it triggered a subtle migration of users to other platforms like Twitch, Among Us and Minecraft.

Quentin Tarantino is set to release 7 Pulp Fiction NFTs with never before seen content from the film. The NFTs will be built on the SCRT Labs’ Secret Network which will allow for public-facing content as well as ‘hidden’ elements/scenes only accessible to the buyer. Among the secret elements being released are the uncut first handwritten scripts of Pulp Fiction and exclusive custom commentary from Tarantino.

Ironically, founders of the (unofficial) Squid Game cryptocurrency have taken off with $3.38m in “investor” money. Buyers of the SQUID token saw the price surge from $38 to $2,860 in a week, however, platforms such as Pancakeswap were unable to process sales (as the SQUID whitepaper had outlined that the tokens could only be liquidated via a ‘play to earn’ game). The irony - just like the Netflix series - everyone else was left for dead.

Usage of China’s digital Yuan (e-CNY) has amplified 6-fold over the past four months, with a whopping 140 million citizens activating their e-CNY wallets. That’s ~10% of China’s population. Furthermore, corporate e-CNY wallets have hit 10m (from 3.5m four months ago), with total e-CNY turnover hitting $9.7bn thanks to acceptance from 1.55m merchants (utilities, catering, transport, retail and government services).

Both Fortnite (Epic Games) and Yahoo (owned by Apollo) have decided to call time on China this week. Fortnite stopped accepting registrations for new players as of Monday, after launching into the market in 2018 thanks to Tencent (700.HK) who own 40% of the parent company. According to Niko analyst Daniel Ahmad, the game never officially launched in the market and was never ultimately approved by the government. Another hint is in this SCMP report which highlights the “subtle influence” such (Metaverse) platforms may have on a country’s political and cultural security.

Elon Musk’s Starlink (private) has registered in India, with plans to apply for licenses and provide internet and other broadband-related communication services. In India, Starlink plans to “carry on the business of telecommunication services” including satellite broadband internet services, content storage and streaming, multimedia communication, among others, according to the company filing.

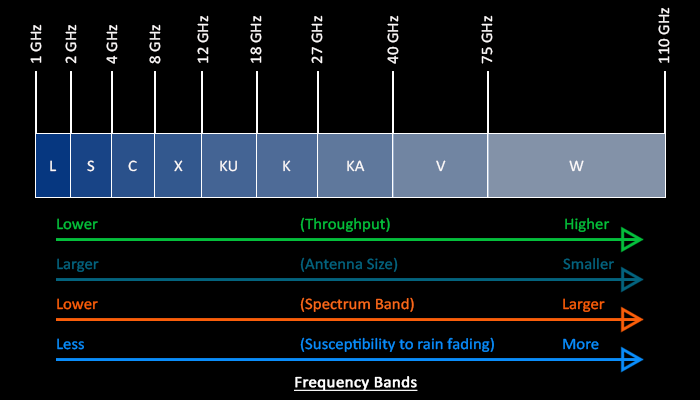

Boeing (BA) has been given the green light from the FCC to operate its own broadband internet network from space, with plans to place 132 satellites (a fraction of SpaceX and Amazon’ network!) in low earth orbit (~1k kms away) and a further 15 way out in non-geostationary orbit (~30k km’s away). However, unlike Amazon and Space X (ka and ku bands), the Boeing license is for V-band broadcasting, enabling faster data transfer rates (but with a greater risk of interference, highlighted below with reference to “rain fading”).

Home buying platform Zillow (ZG), has plummeted ~40% in the past week after ditching its house flipping unit iBuying. In essence, iBuying is/was a C2B2C platform, much like Carvana (CVNA) which buys property (instead of cars) directly off the owner, refurbs it, and then flips it to buyers on the same platform. The intention here is that Zillow had a huge data set and they had hoped this would give them the advantage in identifying arbitrage opportunities where they could consistently flip property for a decent margin. The problem, however, is that the business model proved “too risky, too volatile to (Zillow’s) earnings and operations, too low of a return on equity opportunity and too narrow in its ability to serve customers”. In particular, the pandemic threw their little predictive model out the window! Competitor Opendoor (OPEN) dropped 16% off the back of the news.

Sweden’s autonomous freight company Einride (private) is expanding into the US market, with plans to run tests of its autonomous pods, electric trucks and operating system in partnership with GE Appliances, Bridgestone and Oatly. Unlike autonomous trucking companies like Kodiak and TuSimple, Einride’s pods (below) are cabin-less, meaning there is no intention of having human operators. The immediate use case is more around short-haul trips (i.e. within a port terminal) but inevitably this could be broadened into longer haul. Kodiak and TuSimple’s solution is more around supporting the driver with autonomous solutions (i.e. automation can be engaged on long, less complex routes, but the driver re-engages at points of congestion).

Toyota (7203.JP) have released details of their first mass-produced EV, the bZ4X SUV, which they hope can take on Tesla’s Model Y and Hyundai’s Ioniq. The car will launch in Europe at the end of the year, with this being the first of an anticipated 70 EVs to be rolled out by 2025. Subsidiary Subaru, who helped develop the bZ4X, will release their own EV next year. Both the front-wheel and all-wheel-drive versions are expected to have a range of ~500kms (with up to 80% charge in 30mins). Unique to this EV is the addition of solar panels, which will allow for the car to be charged whilst parked.

Wrapping up this week with some social media updates.

Twitter (TWTR) is expanding its Spaces (clubhouse-esque) feature to allow for hosts to record and share the broadcasts; enabling instant podcast functionality. Meanwhile, Pinterest (PINS), fresh from being stood up by PayPal, have launched shoppable videos with a new feature called Pinterest TV. The videos (example below) allow viewers to watch a range of shoppable videos across themes like food, home, fashion, beauty and DIY (i.e. you could be watching a Martha Stewart video and instantly buy her Vitamix mid-stream).

Earnings

A mammoth week in earnings, from which I’ve picked some notable performers (and notable underperformers). The broader list below is sorted in order of weekly price change (the best indicator of how the market perceived the results!) vs the % that the company beat or missed the analyst’s estimates.

Let’s start with a few notable performers:

Avis (CAR): Stock went ballistic this week, up over 100% after it blew the lights out with earnings. Revenues surged 96% to $3bn (vs $2.7bn estimated) whilst earnings came in at $10.74/share (vs $6.52 estimated). However, a major contributor to such a major price move was the old short squeeze. Approximately 21% of the company’s stock is shorted (i.e. people betting that the stock is going to collapse), however, as the price rallied off the back of positive earnings, those short-sellers are forced to hand that stock (which they’ve borrowed) back!

Hertz (HTZZ): Revenue surged with a recovery in travel, with EPS beating street forecasts by 29%. Profit for the period hit $571m (from a $222m loss a year ago). The company is also still riding a wave of strong momentum following last week’s Tesla announcement.

Ford (F): Not a name you’d expect to see smash earnings estimates, but the big incumbent auto manufacturer completely surprised the market. Although revenue was in-line, the bottom line EPS numbers hit 51c vs street estimates of 27c. On top of that they said they’d reinstate their dividend (after suspending it due to Covid) and raise their full year earnings guidance. Much of this is due to demand for the Bronco SUV and fully electric vehicles, the Mustang Mach-E and Ford F-150 (the latter surpassing 160k reservations).

Matterport (MTTR): Leading “spatial data” / digital twin platform for real estate, architecture and insurance saw 116% growth in subscribers to 439k, leading to a 36% jump in subscription revenue (to $16m) and annual recurring revenue of $63m. On the top line, this was a 25% beat vs street forecasts. Check out the clip below to learn a little more about how this company operate.

Zebra Technologies (ZBRA): Zebra, one of the leaders in industrial / warehouse automation (and a huge investor in industrial automation tech/robotics) , beat estimates across the board with sales hitting $1.44bn and earnings touching $4.55/share.

Shopify (SHOP): Despite missing street estimates, Shopify held up post results with investors bullish on the company’s medium-term initiatives such as international expansion and Shopify POS alongside the more ambitious longer-term strategies relating to Shopify fulfilment network.

….and the underperformers of the week:

Zendesk (ZEN): The provider of customer support services had a bit of a doozy with this quarter’s earnings, missing street revenue estimates by 15%. At the same time, they announced the acquisition of Momentive Global (MNTV) and its SurveyMonkey platform.

Match Group (MTCH): A lacklustre reception from investors as the dating platform pulled in sales in-line with expectations. Tinder revenues jumped 20% year on year, whilst non-Tinder brands grew 32%.

Listings

Amazon’s (AMZN) 20% owned Rivian (private) plans to raise $8.4b in an IPO set to value the EV manufacturer at ~$60 billion - instantly putting it within arm’s reach of GM and Ford’s market cap!

They’re joined by nanosat startup Terran Orbital (private) who are aiming to merge with Tailwind Two Acquisition Corp (TWNT) in a deal valuing the company at $1.6bn. Strategic investor Lockheed Martin (LMT) will be trumping up some of the capital, which will go towards the development of a 660k sqm mega satellite factory in Florida (expected to churn out 1,000 satellites and spaces vehicles annually)! According to the company’s investor presentation, they’re expecting to hit revenues of $918m in 2026 (from a pretty low base of $35m in revenues this year). The superiority of their solution is outlined in the slide below where the planned constellation configuration, size and mass (as well as average revisit rate) puts it above and beyond other providers (particularly relating to US Government related contracts).

M&A | Capital Raise

Nuro (private), the leading autonomous solution for last-mile delivery, has pulled in $600m in funding from Tiger Global and Google, bringing its valuation to $8.6 billion. In addition to the funding, Nuro also announced that they have entered into a strategic five-year partnership with Google to support the “massive scale and capacity required to run self-driving simulation workloads”. The two organisations will also explore other commercial opportunities to “strengthen and transform local commerce”.

As good as satellite solutions are, sometimes having the data on the ground (or in this instance, on the ocean) is the preferable option. This is where Sofar Ocean (private) steps in. Having just raised $39m, the company will be rolling out thousands of smart buoys to scale up its vision of real-time understanding of the world’s seas and oceans. The advantage of sea-level sensors is that granular data on currents, temperature, weather and so on can be pushed through to shippers, government and a range of other customers on a timely basis.

Have a great week.

Charlie

LinkedIn or E-Mail (cnave@granitebaycap.com)

Granite Bay Capital is an innovation focussed investment company with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author(s) and do not constitute financial advice.