Weekly Innovation Review (WIRE) #62

Latest News from the World's Leading Innovators

China Restricts Chip Materials, US Considers Restricting the Cloud

Just moments away from Janet Yellen’s visit to Beijing, China has decided to fire a shot in the ongoing chip wars……..restricting the export of core minerals (gallium and germanium) for use in chips, EVs and select telecom products.

According to the US Geological Survey, China currently accounts for 98% (~430k kgs) and 68% (~140k kgs) of global production in gallium and germanium respectively.

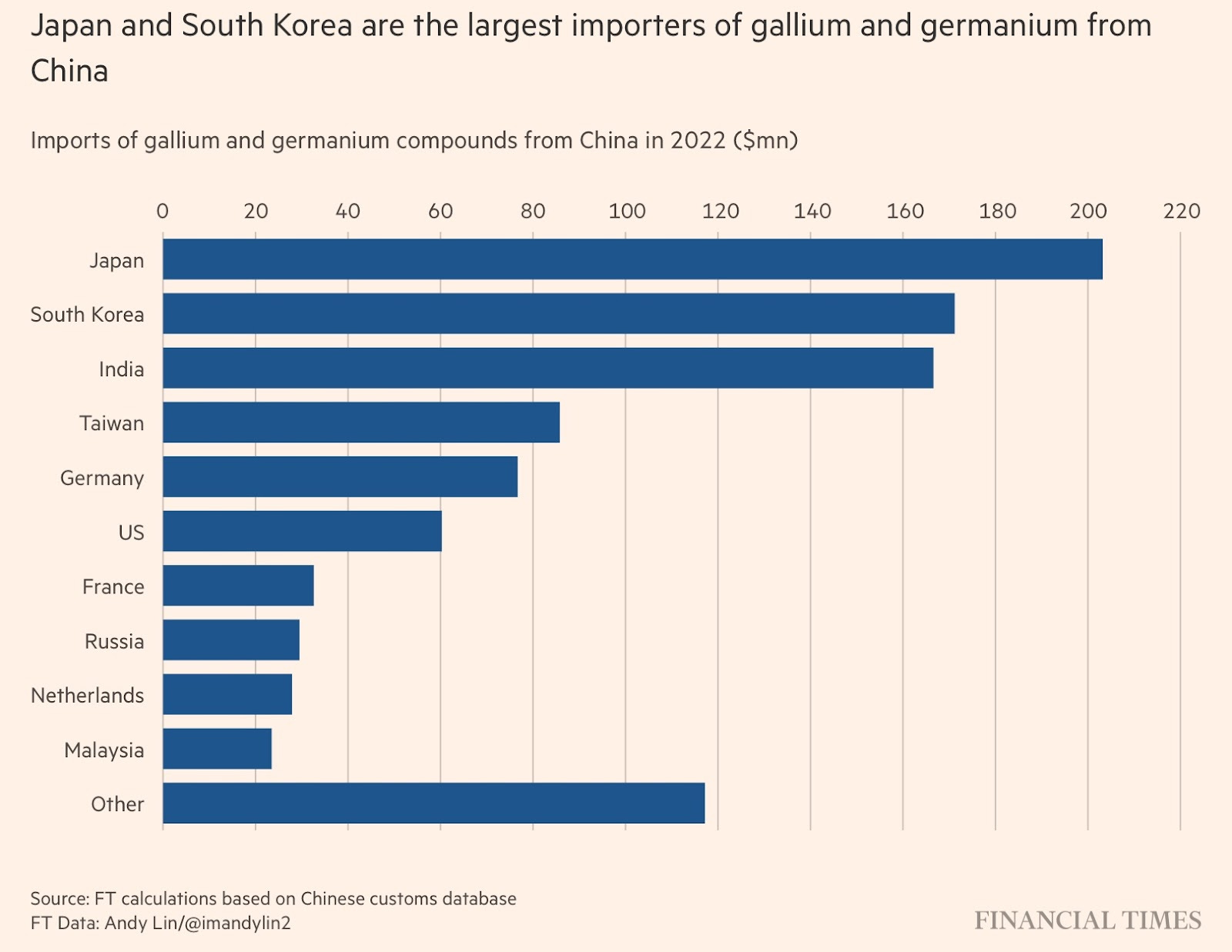

Governments in Japan, South Korea and the US have all expressed concerns, with Taiwan’s deputy foreign minister, Roy Lee, saying the export controls “will be a kind of accelerator for countries including Taiwan, South Korea and Japan to reduce our dependence on China for supplies of those critical materials”.

Such dependence can be seen in the below graphic (Source: FT).

Further, we are seeing signs that the US will restrict China’s access to US cloud computing services (AWS, Azure, Google) where those services would give China access to advanced chip capabilities. The new rules would force the major cloud companies to seek approval before offering those services. China of course has access to Alibaba and Tencent cloud services, however, those companies are heavily restricted in their ability to use the advanced AI chips offered by the likes of NVIDIA.

This tit-for-tat will likely see China retaliate with further measures, which I would expect to extend to other resources in which they have a dominant position….such as rare earths and processed minerals such as lithium, cobalt and graphite, in which China has a dominant market share.

In a prior article I wrote about the opportunity for countries like Australia to fill that gap (in that instance, lithium processing) dominated by China.

In the current context, there are also big opportunities. Gallium is a byproduct of bauxite and zinc. At present, Australia is the largest producer of bauxite in the world, with Rio Tinto and Alcoa being dominant miners. For zinc, China is the dominant producer (~4.2mt), however, Australia is still sizable with production sitting at ~1.3mt (Glencore, New Century and South32 are notable producers).

Australia does have a ‘vision’ for critical minerals, with both gallium and germanium being rated as ‘high’ potential critical minerals along with 14 other minerals. Such moves by China will only catalyse the development of such visions, but it will take time, and considerable investment (South Korea and Japan would be incentivised to invest alongside producers and the Government).

In summary, despite the pain of this China-US battle, it does provide considerable opportunities for nations like Australia to take advantage of tense geopolitical situations by investing in its downstream processing.

India’s Stepping Up to the Chip Plate

India is another huge beneficiary of the above geopolitical situation, with many semiconductor and electronics companies looking to the nation as a way of diversifying supply chain risk away from China.

The country is expected to open its first chip assembly plant next month and break ground on the country’s first fab by the end of 2024, according to the FT. Micron is establishing a $2.75bn chip assembly and test facility in Gujarat (with construction starting next month) thanks to incentives from the Indian government. Due to the considerable investment, such development is only really possible with Government support (look at the US and Germany as an example).

In an interview with the FT, India’s minister for electronics, Ashwini Vaishnaw, says they are in discussions with “14-odd companies” with two of them being rated as a good chance of receiving government support to establish a physical presence in India. It’s unsure where in the supply chain this investment is, but there are positive signs that India will be able to gain some decent traction in securing deals, particularly at the low-mid end of that supply chain.

This is because there are degrees of difficulty across the semiconductor supply chain which are only compounded as you progress. For example, testing and assembly is considerably less sophisticated than manufacturing 40nm chips, which itself is considerably less sophisticated than most advanced 4nm chips.

But this shouldn’t be seen as a problem, because India stands to gain significantly if they can start to build economies of scale in the low-to-mid end of the supply chain over the next couple of decades.

Money (and Moats) Grow in AI

Venture capital and big tech have been opening their cheque books for big AI raises this past week. This will clearly continue to be a theme over the coming year as all of the majors jostle for position as they seek to strengthen their AI foundations.

Firstly, there’s a $1.3bn raise by Inflection AI, a startup founded by DeepMind co-founder Mustafa Suleyman which is making a more personal AI off the back of its Inflection-1 LLM. This AI, which is “designed to be empathetic, useful and safe” brings in capital from Nvidia, Microsoft, Bill Gates, Reid Hoffman and Eric Schmidt, valuing the company at $4bn.

On the Nvidia side, the company says it is working with the company (and CoreWeave) to build the largest AI training cluster in the world - comprising 22,000 Nvidia H100 GPUs! Note, this also comes as we learn that Nvidia had acquired OmniML back in February - a platform which shrinks machine learning applications for use on edge devices (e.g. mobile phones, routers). For Nvidia that’s particularly useful given their already dominant position in powering autonomous vehicles.

Despite pulling in a fraction of Inflection’s raise, with a $141m Series C, it is certainly worth mentioning Runway.

Runway have built and are building AI capabilities which will enable creatives - producers, brands, agencies etc to produce video from text, as well as images and other creative assets. They already count Google, New Balance, Microsoft, Ogilvy and CBS as customers and, through the last capital raise, have added new investors Salesforce, Google, Nvidia and VC firm Rogue.

It may be hard to see, but in the screenshot below, the Runway AI can take reasonably basic text prompt “a palm tree on a tropical beach in the style of professional cinematography, shallow depth of field, feature film” and create very high-quality output, seamlessly. In the words of a CBS customer, this has the power to reduce production time from hours to minutes.

Of course, these investments are also telling us one thing…. the pendulum is swinging more and more towards big tech and that moat between the haves and the have nots is getting bigger. All of this will make it increasingly difficult for independent ventures to compete (i.e. extraordinary high capex, R&D costs, margin pressures etc).

An updated version of the AI ecosystem, encompassing these deals, is available to view and download here.

Meta Coming for Twitter

Meta is launching a new app called Threads, which will be a Twitter-esque “text-based conversation app”. The launch comes amidst increased backlash from the Elon Musk owned Twitter and is in line with the company’s strategy of hitting product “parity” with a number of rival platforms like TikTok, Snapchat and Discord.

Since Musk’s takeover of Twitter, he has driven a lot of division amongst users. This stems from revisions to verification and content moderation policies, drastic headcount reductions, system outages and, most recently, access restrictions.

Let’s see if Meta can succeed where others (i.e. Truth, Bluesky and Mastodon) have failed!

Thank you and have a great weekend ahead!

Charlie Nave

LinkedIn or E-Mail (cnave@granitebaycap.com)

Associate Professor (Practice) Monash Business School and Monash Centre for Financial Studies (MCFS)

Granite Bay Capital is an innovation focussed consultancy with a deep focus on the companies at the leading edge of innovation across major themes such as AI, ubiquitous computing, sustainability, automation and longevity. Any views expressed in this article are those of the author and do not constitute financial advice.